Securing a car loan is an exciting but important step toward buying your next vehicle, but the process can from quick & easy, to slow and painful quickly if you are not properly prepared with the right documentation.

Having a complete set of documents is essential to keep the process smooth and stress-free.

Not only does this demonstrate your credibility to the lender, but it also accelerates approval times. Let’s explore why being organised with your documentation is the secret sauce to a hassle-free car loan experience.

Key Takeaways: Document Checklist

| Document Category | Document Required |

|---|---|

| Identity & Address | Verifies identity (100 points of ID) and current residential tenure. – Driver’s License, Passport, or Birth Certificate. – Recent utility bill or council rate notice. |

| Income & Employment | Prove consistent earnings and ability to comfortably handle the loan repayments. – 2 most recent recent Payslips – Notice of Assessment (NOA) to evidence overtime or bonus income – Letter from employer (rarely required). |

| Financial Health | To assess current cash flow, spending habits, and remaining borrowing capacity. – Details of all existing debts (credit cards, personal loans, etc.). – 90 days of Bank Statements (only required in some circumstances). |

| Vehicle Details | Purchase agreement/quote (new car) or Rego certificate & Roadworthy Certificate (used car). |

| Proof of Insurance | Certificate of Currency to evidence Comprehensive Car Insurance is usually mandatory for a secured car loan. |

Legal Obligations: Why Lenders Require Documentation

The short answer is government regulation. Most lending activity in Australia is heavily scrutinised to ensure that consumers are treated fairly and responsibly while also protecting the system from illegal conduct.

The two primary pieces of legislation that influence the documents you need to provide are:

- Responsible lending obligations under the National Consumer Credit Protection Act (NCCP)

- Anti-Money Laundering and Counter-Terrorism Financing Act (AML/CTF)

While you may have little interest in the details, it may at least help you understand why there are such rigorous standards.

The basic principles are not to lend money to people who cannot afford it and do not lend money to facilitate criminal enterprise.

How a Good Broker Can Simplify the Documentation Process

Through the use of technology, you can now submit a number of these documents digitally and within seconds.

You no longer need to print physical copies and have them certified by a JP, as may have been the case in years gone by.

Here at Gusto Finance, we prioritise digital submission of ID, bank statement data, and various other contracts and disclosures so you can navigate the process as quickly and easily as possible!

Categories of Required Lender Documentation

Most Australian lenders ask for documents to verify:

- Identity

- Residential status

- Income & Expenses

- Outstanding loans or other liabilities

- Credit History

- Other financial obligations

These documents help them assess whether you’re capable of repaying the car loan and minimise risk for the lender and ensure a transparent process for both parties.

1. Identity Verification: Primary & Secondary ID

To confirm your identity, lenders require government-issued documents. This step ensures that you’re a legitimate applicant and not attempting fraud.

The latter may sound silly, but identity theft and scams are increasing at a frightening speed. So it is a necessary inconvenience to ensure that you do not become the victim of such a scheme.

Commonly Accepted Forms of ID in Australia

There are two categories of identification typically required to verify your identity, primary and secondary.

Both carry different weights to satisfy the minimum requirements (usually 100 points of ID) and each lender may have different policies for what is acceptable.

Primary:

- Driver’s license

- Passport

- Birth Certificate

- Citizenship Certificate

- Proof of Age Card

- Immigration Card

Secondary:

- Medicare Card

- Bank Card

- Utility Bill

- Rates Notice

- Student Card

- Employment Document

- Overseas ID

You should ensure that the ID you provide is current and matches your application details to avoid the need for additional documentation.

2. Income Verification: Payslips, Tax Returns, & Self-Employment

Lenders need to be confident that you can repay the loan. Your income is one of the biggest factors in assessing your repayment capacity.

They’ll look for consistent earnings over time to gauge your financial stability. This can be more difficult for those who are self-employed or run a business, so we will address this in two sections.

Payslips, Tax Returns, and Other Proof of Earnings

If you’re employed, recent payslips (usually the last two to three) and your most recent tax return are standard requirements.

If your income fluctuates due to bonuses, overtime, or any other type of irregular earnings then you may need to show your annual tax assessment for up to two years. These are available online via the ATO website.

For additional assurance, some lenders may request 90 days’ worth of bank statements. This will help verify both your income and expenses (which we will get to shortly).

The quickest and easiest way is to submit your statements digitally through something called Screen Scraping. This is an online portal where you log into your online banking and have the data in your statements scraped in seconds.

It is the fastest and easiest way, and increasingly becoming a requirement of lenders.

What to Provide If You’re Self-Employed

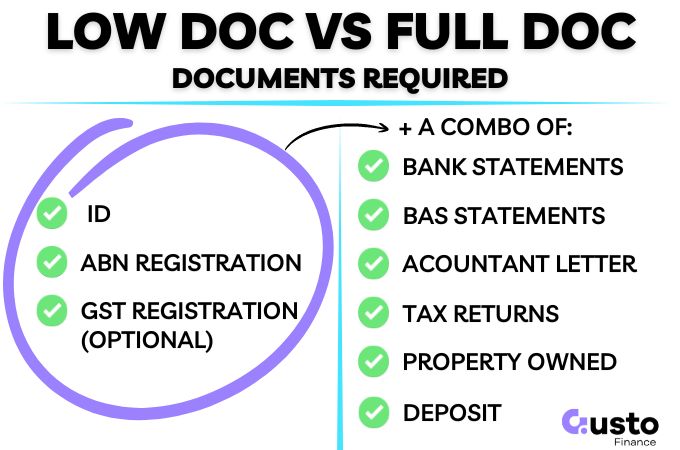

ABN holders have some options here. The quickest and easiest is to go for a low-doc car loan.

You may not have to provide proof of income (in some circumstances) at all with only the following documents for a low doc car loan application being required:

- ABN registration (>6 months old)

- GST registration, if applicable

However, a full-doc loan business loan is another option that is more detailed compared to low-doc.

This could require more extensive documentation, including:

- Business Activity Statement (BAS)

- Profit & Loss statement

- Annual Tax Assessment

- Letter from an accountant

- Business Bank Statements

3. Confirming Employment Stability & Tenure

If you have submitted bank statements then this will often be sufficient to verify your ongoing employment. However, in some circumstances, you may be required to provide more information.

Verification Letters and Employer Details

Some lenders will contact your employer to verify your position, tenure, and salary. Especially, if you have only worked with your employer for a short time and may be subject to a probationary period.

A formal letter from your employer can help speed up this verification step.

Explaining Gaps in Your Employment History

If you have periods of unemployment, be prepared to explain them.

Supporting documents, such as Centrelink statements, can help clarify your financial stability during these times.

It is always helpful to declare these things upfront and provide documentation to support your explanation. The lender is obligated to question these things and it will only slow down your car loan assessment if you try and avoid them.

Proof of Address

The following documents are acceptable proof of residence for a car loan:

- Utility bills

- Rental agreement

- Bank statement

- Council rate notice

Where you may get into trouble here is if you have moved house recently, or have just forgotten to update your addresses (something I am frequently guilty of!!).

Most of this information can be updated quickly online without the need to sit on the phone for hours so it is always best to keep up to date and well before you want to apply for auto finance.

These documents should show your name and current address.

Why Your Residential Address Is Important

Confirming your current address is critical for the lender to be able to send you the statements, notices, and other legal documents that are required by law.

Time at your current address and stability of residential history is also something that is considered as part of your application.

So be prepared to provide your full residential history for at least the last two years, and sometimes beyond.

4. Credit History: Assessment and Accessing Your Report

Your credit history tells lenders how you’ve managed debts in the past and is one of the most critical factors in assessing you as a credit risk.

A strong credit score can lead to better interest rates and loan terms, while a poor score may be more costly or require additional guarantees.

However, there are plenty of lenders who specialised in second-chance car loans and you may be better placed than you think if you have missed payments in the past.

Get in touch with our expert brokers below for a complete assessment of your options.

How to Access Your Australian Credit Report

The good news is that you don’t need to get this yourself. When you apply online our system will automatically retrieve your credit report so we can match you with the right lender.

This is done in a way that does not impact your credit score and no marks are left until you submit a formal application to a lender.

However, if you want to see your credit file for yourself there are a number of ways to get a copy for free! You can register for your free credit file at any of these Credit Bureaus:

Reviewing your report beforehand can help you address any inaccuracies or issues.

If you also want extra protection from identity theft you can pay to monitor any activity on your credit file. You’ll be notified of all activity, which allows you to proactively intervene if you notice things not initiated by you.

5. When Bank Statements Are Required

We have already discussed this with regard to the speed and convenience of screen scraping, but I wanted to share a little more detail on the importance some lenders place on bank statements.

It is worth noting that the majority of car loan applications do not require bank statements.

Why Lenders Want to See Your Bank Transactions

A lender will only require bank statements when there is a specific reason to scrutinise these further. For example, a low credit score that falls below a certain threshold.

Bank statements provide a snapshot of your financial health, showing your income, expenses, and savings habits.

They help lenders determine whether you can comfortably handle loan repayments, what portion of your expenses are essential, and what is disposable (discretionary expenditure).

The latter can be changed to meet loan repayments, which can be important when deciding if you can afford your loan repayments.

Lenders that specialise in car loans for people with bad credit will place much more emphasis on your money management, and your bank statement data may be the biggest influence on whether you get approved or not.

How Many Months of Statements Are Typically Required

Lenders usually request statements for the past three months. It would be rare for six months to be required unless you were going for a much larger loan or a mortgage.

Ensure these show consistent income and responsible spending and you will present much better to the lender… Now might be a good time to cancel all those unused streaming subscriptions!!

6. Declaring All Debts and Financial Liabilities

Loans and Credit Cards

Transparency with your existing loans and credit card debts is crucial.

Lenders will already see evidence of these from your credit file and bank statement data, but may request documentation showing:

- Personal Loan: Repayments, remaining balance, and loan term.

- Credit Card: Your minimum repayments and credit limit.

This information will help the lender assess how much of your income is left over to make repayments on a new car loan.

All debts you have outstanding will directly reduce your borrowing capacity. Conversely, a manageable debt load signals financial responsibility.

Other Financial Commitments

If you have other ongoing commitments then also be prepared to disclose these and provide documentation to show the size and duration of your required payments:

- A tax debt to the ATO

- Centrelink debt

- Child support payments

- Unpaid bills that are on a payment plan

Accurately declaring a list of dependents is also an important one. While a lender is unlikely to ask for specific documentation, when they look at your bank statements they will know if you have undeclared children.

7. Vehicle Documentation: New, Used, & Private Sales

This will vary depending on whether it is a new or used car, a private sale, or through a dealership.

Documentation When Buying a Brand-New Car

When purchasing a new vehicle, a purchase agreement or quote from the dealer is typically required.

This document outlines the car’s price and specifications.

Documentation When Buying a Second-Hand Car Purchase

For used cars, you’ll need the seller’s details, the vehicle registration certificate, and a copy of the roadworthy certificate.

Lenders may also request a valuation report to verify the asset details.

Dealership or Private Seller

If you are buying privately you will have to source most of these documents yourself. Which will add a bit of legwork and inconvenience.

A dealership will have done this a thousand times and will have most documentation ready to go for you.

8. Guarantor Documentation

A guarantor may be needed if your credit score or income doesn’t meet the lender’s criteria. This is most common among younger people who have not yet built up a sufficient credit history to take out a large car loan.

This guarantor agrees to take on the loan’s responsibility if you default.

Car Loan Guarantor Document Requirements

Guarantors will need to supply all of the same documentation as the primary borrower; identification, proof of income, and a credit history report.

They’ll also need to sign a legal agreement outlining their obligations in the event the primary borrower defaults and does not repay the loan.

9. Proof of Deposit or Down Payment

Lenders often ask for bank statements or receipts showing your deposit amount. This assures them that you’re financially invested in the purchase.

What Counts as a Valid Down Payment Proof

Acceptable proof includes bank transfers, savings statements, or a cheque copy. Cash payments may require additional evidence.

10. Car Insurance Requirements

Why Comprehensive Insurance Is a Must in Australia

Lenders typically mandate comprehensive car insurance to protect their investments. This ensures the vehicle is covered in case of accidents or theft.

When to Provide Proof of Insurance

You’ll need to present insurance details before the loan is finalised or at the time of vehicle delivery.

11. Residency and Visa Status

If you are new to Australia or are here temporarily then it will be more difficult to get a car loan. However, there are a number of lenders who will accommodate a range of scenarios.

Documents Required for Non-Citizens Applying for a Loan

Non-citizens must provide:

- Visa details – the class of visa may determine eligibility

- Length of stay

- Residency proof

- Employment documentation

Permanent residents often face fewer restrictions than temporary visa holders for obvious reasons. If you are on a visa then get in touch with our brokers to discuss your options.

Top Mistakes to Avoid in Your Loan Application

Remember that lenders have a legal obligation to assess your finances thoroughly, and they will be liable if they do not adequately complete this.

So, it is your responsibility to ensure that the documents are complete and accurate. Do not expect any flexibility.

Here are some of the more common mistakes that borrowers make when compiling the documents they need for a car loan:

Outdated Documents

Every lender will have a strict date policy, which will also vary by the type of document.

For example, a payslip must include your most recent payslip. Whereas a rates notice for proof of address could be up to three months old.

Always aim for the most recent version of the document you have.

Missing Documents

Double-check your checklist to avoid delays caused by missing paperwork.

Your broker, or lender, cannot complete a submission or assessment until all documents are there.

In the past I have submitted most of the documents so they can get started on the assessment, thinking it would save time…. It doesn’t! You need it all before work will begin.

At Gusto Finance, we provide you with a checklist so you know exactly what you need and can tick them off one at a time.

Providing Incorrect or Incomplete Information

Ensure all details are accurate and up to date. Inconsistencies can raise red flags for lenders.

Attempting to Hide Information

Lenders have sophisticated systems that detect payments and items on your credit file, and they all need to be explained.

If you try and outsmart the lender you will either slow down your application or end up being declined for your loan – which will leave a mark on your credit file and make it harder to apply elsewhere.

So be honest, and be upfront.

If you suspect there are problems that may prevent you from being approved then speak with one of our brokers. We have access to over 30 lenders and can match you with the lender that could accommodate your specific situation.

What to Do If You’re Missing Documents

Steps to Take If a Document Is Lost or Unavailable

Contact relevant organisations (e.g., the ATO or your employer) to request replacements. Acting promptly prevents delays.

Alternative Evidence Australian Lenders May Accept

If a standard document isn’t available, lenders may accept secondary evidence, such as statutory declarations or additional verification letters.

Final Checklist for a Fast Car Loan Approval

Preparation is the cornerstone of a successful car loan application.

By gathering all the necessary documents and staying organised, you can minimise stress and get on the road faster.

With everything in place, you’re just steps away from driving off in your dream car.