If you are wondering if you can get a boat loan with bad credit, the short answer is yes.

While your options will be more limited than a prime borrower, approval is absolutely possible.

It depends on your current affordability, the lender’s specific guidelines, the vessel itself, and the rate you are prepared to tolerate.

When applying with a lower credit score, you can expect fewer lender options, higher interest rates, and stricter loan conditions.

However, past financial mistakes can be overcome if you know where to look.

In this article, we cover exactly how lenders assess bad credit applications, highlight hidden deal-breakers (like vessel age, private sales, and marine surveys), and detail the steps you can take today to maximise your approval odds.

Key Takeaways: Bad Credit Boat Loans

| Approval is Possible | You can secure a loan through specialist non-bank lenders if you can demonstrate clear affordability and clean recent banking conduct. |

| Expect Higher Pricing | You will pay higher interest rates and fees. Always compare using a broker so you can get the best deal for your credit profile. |

| Asset Quality Matters | Lenders assess the asset alongside your financial profile. They can decline an application based purely on the vessel’s age, condition, or market value. |

| Private Sales Add Hurdles | Buying privately restricts your choice of lenders and triggers strict paperwork requirements to prevent fraud. |

How Lenders Define Bad Credit

A bad credit rating is simply a mathematical calculation of lending risk (e.g. how likely you are to pay the lender back).

A higher risk profile immediately translates to fewer lender options and higher interest rates.

Lenders generally group credit-challenged applicants into three distinct buckets:

- Low credit score: Driven by past repayment issues, unpaid defaults, or heavy credit-seeking behaviour (applying for too many loans at once).

- Thin credit history: Having limited file data because you are young, new to Australia, or have simply never taken out a major loan before.

- Poor money management: Lenders heavily scrutinise your recent bank statements for risky behaviours like overdrawn accounts, late fees, or direct debit reversals.

Boat finance also carries a unique nuance. Even with a perfect credit score, marine lenders treat boat applications as slightly higher risk than cars.

A vessel is a luxury lifestyle asset, making it harder to value and sell if the loan defaults.

The Reality of Bad Credit Boat Approvals

A past financial mistake does not mean an automatic decline. A bad credit score can be overcome if your current affordability and recent banking conduct are strong.

Because mainstream banks have a limited appetite for risk, securing approval requires navigating specialist non-bank lenders.

These lenders will take on impaired credit, but they price that risk into the loan.

| Metric | Prime Boat Loan | Bad Credit Boat Loan |

| Interest Rates | Lower | Higher (Risk-based pricing) |

| Lender Options | Major banks & marine specialists | Niche non-bank lenders |

| Upfront Fees | Standard establishment fees | Higher risk and establishment fees |

| Maximum Loan Term | Up to 7–10 years | Often capped at 3–5 years |

| Deposit Required | Often 0% required | Larger deposit sometimes requested |

The biggest mistake you can make is applying everywhere in search of a lender that will consider your profile.

Multiple formal applications create multiple hard credit enquiries.

This further damages your score and triggers instant rejections. Instead, use a broker to check your eligibility before submitting a full application.

Why the Boat Itself Can Cause a Loan Decline

If the lender instantly rejects your application the boat itself could be the problem, not just your credit profile.

Boat loans work in a similar way to a car loan where lenders have strict criteria for what they will accept as security.

Criteria often centres on the boat type and age.

Older vessels often trigger stricter loan conditions, such as shorter repayment terms, larger deposit requirements, or being restricted entirely to an unsecured personal loan.

Some lenders also have further restrictions on private sales.

Additional verification work is required to prove no existing finance is owing on the asset. A clean PPSR search and a perfectly accurate HIN are absolute requirements.

Furthermore, for older or high-value used boats, expect to pay for a formal marine survey.

Any structural issues uncovered during this inspection will change your approval conditions.

To avoid pursuing an unfinanceable boat, gather these basic details before starting a formal application:

- Build year, make, and model

- Accurate Hull Identification Number (HIN)

- Agreed purchase price

5 Steps to Prepare for a Bad Credit Boat Loan

Lenders will scrutinise your last 90 days of bank statements to assess your financial capacity and budget management.

Follow these five actions to improve your approval odds before you apply:

- Get current arrears up to date: Clear all overdue accounts. Lenders will automatically decline applicants with active, unpaid defaults.

- Stop wage advance transactions: Delete payday lending apps and pause Buy Now Pay Later (BNPL) usage. These services signal financial stress and breach lender hardship guidelines.

- Eliminate payment reversals: Align direct debits with your pay cycle. Dishonour fees and overdrawn accounts will derail your application.

- Save a cash deposit: Contributing your own cash reduces the total loan amount and offsets the lender’s risk, making them more likely to approve the loan.

- Pick a finance-friendly boat: Target newer, factory-standard vessels with clear ownership records to avoid triggering mandatory marine surveys.

Even if your credit score remains low, demonstrating flawless recent banking conduct proves you can manage a new loan responsibly.

How to Secure Your Bad Credit Boat Loan

Obtain Pre-Approval Before Committing to a Purchase

Applying to multiple lenders directly will damage an already fragile credit file.

Instead, protect your score by using a soft-search eligibility check through a finance broker.

They will match your specific credit profile and boat details to the specialist lenders who actually fund these deals.

By doing this first, the pre-approval locks in a realistic budget so you can search the market with confidence. Allowing you to move fast when you find the right vessel.

A broker will also verify a lender’s private sale policies and maximum boat age limits before submitting paperwork so that you are more likely to secure that final approval once you select your boat.

Get started with your pre-approval by clicking below.

Improve Your Chances of Final Approval

A larger deposit, an improving credit profile, and a solid explanation for problems of the past go a long way when seeking that loan approval if you have bad credit.

A broker can provide this important context along with your application when it goes in for final assessment.

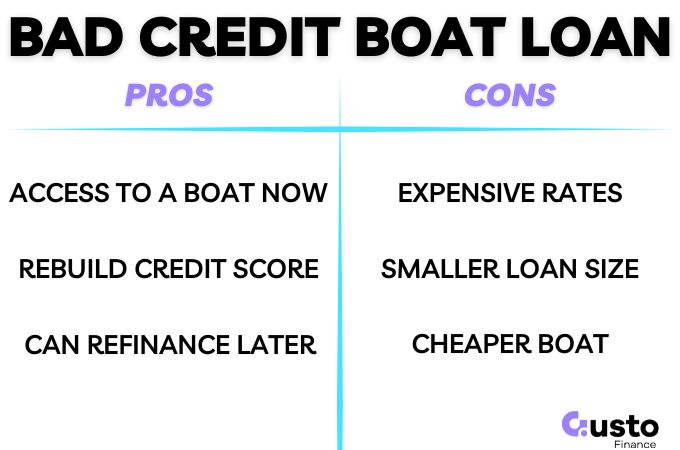

While you may be stuck with a more costly loan for now, you get access to the boat now, and you can rebuild your repayment history over time.

You also have the potential to refinance to a cheaper rate in 12–24 months once your credit improves.

Frequently Asked Questions

Will applying for a boat loan hurt my credit score?

Submitting a formal application records a hard enquiry on your credit file. Multiple hard hits lower your score and signal financial stress to lenders. Protect your rating by using a broker for a soft-search eligibility check, which assesses your options without causing any damage.

Can I get a boat loan with defaults on my credit file?

Specialist lenders will consider your application even with past defaults, provided your recent banking conduct is flawless. However, active, unpaid defaults are usually an instant decline. You must bring all current arrears up to date before applying.

Can I finance a private sale boat?

Yes, but it requires significantly more administrative work than a dealership purchase. Lenders view private sales as higher risk. You must verify the seller’s identity, provide a clear PPSR search, and confirm the HIN.

Do I need a marine survey to get finance?

A marine survey is often mandatory when using an older or high-value used boat as loan security. Lenders require this inspection to confirm the vessel is seaworthy and accurately priced. Always budget time and money for this step.

Your Bad Credit Boat Loan Strategy

Yes, you can get a boat loan with bad credit. Success depends entirely on your lender choice, your recent banking conduct, and the boat’s eligibility.

To give yourself the best chance of approval, halt any high-risk transactions (like BNPL or wage advances), save a cash deposit, and protect your credit file by avoiding multiple formal applications.

Ready to get on the water? Speak to a Gusto Finance specialist today for an obligation free preliminary assessment.

We will quickly match you with the right lender based on your current behaviors, not just your past mistakes.