A self-employed person may not be eligible for a regular consumer car loan in some cases and may be required to get a commercial loan.

Instead of payslips to evidence income, you may have to provide tax returns, BAS statements, and possibly get accountants involved.

But there is an easier path!

In this article, we will discuss exactly what is required to get your car loan approved and what improves your eligibility for finance as a self-employed business owner.

Key Takeaways: Car Loans for ABN Holders

| The Low-Doc Shortcut | Low Doc Loans are the quick & easy car financing solution for business owners. All you need is an ID and ABN. |

| Full-Doc Options | A range of commercial finance products are also available such as a Chattel Mortgage or Hire Purchase Agreement. |

| Required Trading History | For tradies, just one day since registration is possible! For other businesses 6 months is the minimum. |

| Vehicle Use Matters | To qualify, the vehicle purchased must be used for business purposes at least 50% of the time. |

| GST Registration | Most lenders require this as it demonstrates business turnover >$75k per year. Some lenders do not require this. |

Why Self-Employed Loans Are Treated Differently

Your car loan application is either going to be very easy or very complicated. Rarely is there something in between.

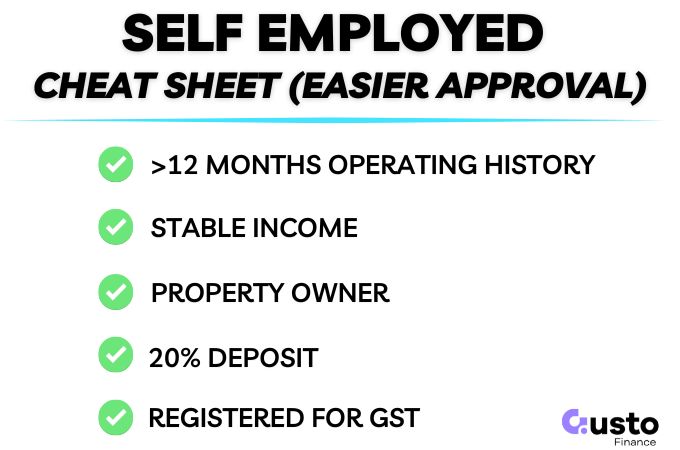

If you are a property owner, have a 20% deposit, and a stable business operating history, you can usually get a low-doc loan very quickly.

Which means you could be approved without having to jump through as many hoops as a full doc loan.

A newer business or a more complex asset to finance may need to provide more detailed business financials to be approved for a car loan.

The cost of the loan may also vary significantly depending on the quality of the underlying business and the strength of the documentation provided in the application.

Car Loan Categories for Self-Employed

The first step for a self-employed person is to decide on the type of loan that would best suit your situation.

This will depend on how your business is set up, how you pay yourself, and your operating history.

Working through a preliminary assessment with an expert broker will shortcut this process and ensure that you are on the right track early.

Submit an enquiry below and our team will be in touch.

Option 1: Low Doc Loan

It is common for self-employed people to be unable to demonstrate regular earnings in the same way as a PAYG employee.

A low doc loan can simplify the pathway to a loan approval. In some cases it can be as easy as providing your ID and confirming business registration.

Some lenders may ask for additional information such as:

- Proof of ownership for property or other assets (e.g. a rates notice).

- Business Activity Statements (BAS)

You could also have your loan assessment completed in minutes rather than days, depending on the lender you are placed with.

It is the quickest and easiest pathway to a loan approval. But there is a downside.

From the lender’s point of view, this category of car loan is more risky due to the lack of earnings stability and lower threshold for documentation provided.

So expect to pay a higher interest rate.

Option 2: Chattel Mortgage

These are the same as a consumer car loan in form and substance, but are used when financing a commercial asset.

In order to qualify, you must be purchasing a vehicle that will be used predominantly for business purposes.

Think of a tradie’s ute, a removalist truck, or a car for a traveling salesman.

The business owns the vehicle but uses it for security against the loan. The lender registers an interest (or mortgage) over the asset.

In the event of non-payment, the lender can repossess the vehicle in a similar way to a regular consumer loan.

There are considerable tax advantages to this type of loan. Deductions related to depreciation and interest can be made, plus GST credits are also available.

Option 3: Commercial Hire Purchase

The main difference under a hire purchase agreement is the lender owns the vehicle until your payment of term is complete.

You hire the vehicle from the lender and make payments to them in much the same way as you would as a regular loan.

At the conclusion of the agreement, the ownership then passes over to you.

Eligibility for a Self-Employed Car Loan

Trading History (ABN Length) Requirements

You only need your business has been registered for 6 months to qualify for some commercial car loans.

After 12 months you will have many more options available to finance a commercial vehicle.

As mentioned earlier, there is an easy path and a difficult path. But one of the benefits of commercial lending is that there is more wiggle room for a bespoke solution that fits your profile.

Especially if you are a property owner and willing to provide a director’s guarantee.

So rather than discuss the extensive shades of grey, it would be best to focus on the documentation you can prepare to ensure that you are presenting your business accurately.

Documentation Required

The required documents will vary depending on your situation and the category of loan you are applying for.

A borrower must still demonstrate sufficient income to repay the loan and general financial responsibility.

But the sources required to support this are very different from consumer loans and may include:

- ABN registration

- GST registration

- Accountant letter

- Business Activity Statements

- Up to 6 months of business financials

- Tax returns (up to two years)

- Evidence of cash to be used for a deposit

- Details of property owned

While not all of the above apply to every self-employed car loan, you should prepare as much as you can to speed up the application process.

Selecting the Most Suitable Lender

Highest Chance of Approval

Fewer lenders will accommodate self-employed or business car loans, compared to a regular consumer loan.

The most important part of the process is to identify the lender who is most likely to accommodate your specific situation.

A broker has a working relationship with a panel of lenders and will know who offers the required loan product and the willingness to lend to your customer profile.

Given how individual business-related loan applications are, this inside knowledge can make all the difference.

Brokers also have a direct line to people working within the lender and are able to provide important context to things like inconsistencies in the income demonstrated or one-off expenses.

This ensures a fair and accurate credit assessment.

Lowest Interest Rate and Fees

One you have narrowed things down to a list of lenders that are most likely to approve your application we can now consider the costs associated with the loan.

Commercial rates are generally higher than consumer loans, and they will also vary considerably depending on the loan category and type of vehicle you are financing.

Securing a good rate will depend on the following:

- Stability of business income

- Credit score of the self-employed person

- Size of deposit

- Type of asset being financed

- Whether the loan is to be secured or unsecured

In most cases, it makes more sense to take out a secured loan and take advantage of the lower interest rate on offer.

Unsecured commercial lending can have interest rates attached that will make your eyes water and rarely would we recommend this.

Can New Businesses (<1 Year) Get Approved?

Some new businesses in the trades can get approved for car financing the day after they register their ABN (new rule introduced in late 2025)!

For most other businesses you will require 6 months. You will be relying on non-bank lenders though, as most of the major banks will require over one year of trading history.

These rules are constantly changing so you need an expert broker team on your side to ensure you are placed with the best lender for your self employed car loan.

Preparing to Finance a Car While Self Employed

The best thing you can do in preparation for a car loan application as a self-employed business owner is to keep impeccable records.

As we have discussed, you will need to provide evidence of business income and possibly your full business financials over a long period of time to be eligible for finance.

If your records are a mess, then this will either take up a lot of your time to make them lender-friendly, or a lender may just put you in the too-hard basket.

Going through the preliminary assessment with a broker can help make sure your application is lender-ready before it is passed on and will give you the best chance of securing a great deal!