Nothing will kill your car loan application faster than a high number of gambling deposits to your favourite bookie.

Aussies love a punt! And as long as you gamble responsibly, your application should be unaffected.

However, did you know that cash withdrawals could also be interpreted as gambling transactions? You may unknowingly be waving red flags where there are none.

In this article, we’ll discuss what is considered a gambling transaction by a car loan lender and at what point it may become a problem.

Key Takeaways: Gambling Transactions

| How Will They Be Identified | Some lenders will request to see 90 days worth of bank statements if there is a reason to look closer at your application (e.g., low credit score). |

| Will I Be Declined? | This depends on the amount and frequency of gambling evident in your transaction data. A responsible level of gambling is usually ok. |

| Legal Requirements | A lender can only approve a loan when the borrower can repay without experiencing financial hardship. Gambling could indicate risk of hardship. |

| Lender’s Risk Assessment | A lender also wants to lend to people who are most likely to repay the loan. Problem gamblers may be less reliable. |

| How to Fix Excessive Gambling | The simple answer is to reduce or cease your gambling activity for at least 90 days leading up to your loan application. |

Why Auto Finance Lenders Must Care About Gambling

This only matters if the lender requests to see your bank statements as part of their credit assessment.

Most of the time this is not required, but if you have a lower credit score or some recent arrears on other debts your application may attract more scrutiny.

There are two reasons why a lender will examine any gambling transactions in your bank statements.

Risk Assessment

A problem gambler is less likely to repay their loan on time, and lenders generally have no interest in giving money to people who will not pay it back.

Excessive and frequent gambling is a strong indication that you are not managing your money well.

Lenders will question this when processing your car loan application.

Responsible Lending Laws

Australia has strict rules on who you can’t lend money to. A particularly sensitive part of the credit legislation is in relation to vulnerable consumers.

A problem gambler is considered a vulnerable consumer.

If a car loan is provided to someone who clearly has a gambling problem, then there could be significant penalties imposed by the regulator, and the loan would be unenforceable.

Both scenarios result in significant loss by the lender, and could potentially lead to their credit license being revoked.

3 Signs You May Be Flagged as a Vulnerable Consumer

To be considered a problem gambler and a vulnerable consumer, there must be a pattern evident in your bank statements.

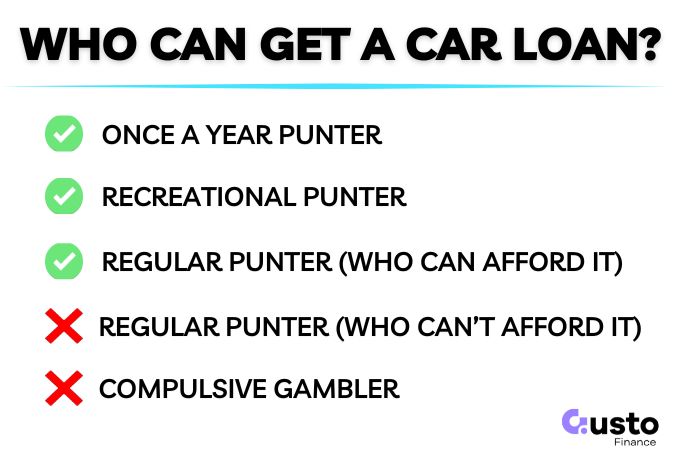

If you like to have a big bet once a year on Melbourne Cup Day, then this will not indicate a pattern – even if you drop half your wage on your favourite horse.

But if you do that every weekend throughout the 90-day statement period, then this could indicate a pattern, IF, you cannot afford this habit.

Let’s consider some common scenarios that may indicate problem gambling.

Sign 1. A Large Portion of Your Income is Regularly Spent on Gambling

Regular gambling is not really a problem if you can afford it.

A high-income earner can gamble more than the average punter without it affecting their ability to meet their financial obligations.

Therefore, lenders will assess the acceptable portion of income very differently depending on your income level.

If you earn $1,000 a week and gamble $500 a week, then this is a big red flag.

Sign 2. Repeated Gambling Transactions in Short Windows of Time

Coming back to our Melbourne Cup Day example. Let’s consider the following sequence of events and how it may appear to a lender:

- You deposit $100 in your TAB account to bet on your favourite horse in the race.

- You get to work and someone has a hot tip in race 3. You deposit another $50 to take that early bet.

- The hot tip loses. You’re already at the pub but have a couple of hours until the big race. Deposit another $50 to bet a few dollars in each race to pass the time.

- A 100/1 shot you have never heard of from Ireland wins the Melbourne Cup. Oh well, you are a few beers deep and having fun. Another $50 goes in to see out the day.

We are now up to four deposits on the day. All harmless fun in the context of Melbourne Cup Day, but remember, a lender doesn’t know the story behind the transactions.

What they see is deposit -> loss -> deposit -> loss… etc.

This is a pattern that could indicate vulnerability. A single day is likely to be fine but what if this is a regular thing?

If this pattern repeats even once a week, you are already getting close to 50 gambling transactions over the 90 days!!

Sign 3. Repeated Cash Withdrawals in Short Windows of Time

Excessive cash withdrawals can be problematic for the same reason as the above example. Just replace the TAB with poker machines.

Have you ever been to an ATM four times in one day? Most people never have, and it would look very strange on a bank statement.

But hang around a pub’s ATM long enough and you’ll see people doing laps between the pokie room and the ATM.

It is in the lender’s best interest to assume the worst when someone is making repeated ATM withdrawals.

Rarely is there a good reason for this behaviour, especially if it is a pattern that repeats itself.

What Transactions Count as Gambling?

Gambling transactions are identified by the merchant information included in your bank statement.

For example, it is easy to see that the transaction below is related to gambling.

- POS W/D Sportsbet Fis-12:13 -$200

Unfortunately, they are not all this easy. I am sure the people of Casino can attest to that (a suburb in Northern NSW if you were not aware).

Gambling Transaction Categories

Below are the most common categories of gambling transactions.

While the intention is to include all transactions where money is spent, where there is a chance of a speculative win, often other things can also be mistakenly included.

- Online bookmakers (over 100 currently operating in Australia!)

- Online casinos

- Lottery tickets (think Powerball, Lotto, Aus Lotto, etc.)

- Cash withdrawals within betting venues

- High-frequency cash withdrawals

It is a constantly evolving space with new betting operators opening frequently.

Incorrect Gambling Transaction Identification

We have already discussed the possibility of mistakes being made – if you live in Casino and use the local ATM then you may get flagged for casino withdrawals!

This is a simplified example of course, most lenders are a bit more sophisticated, but it does demonstrate the risk.

The greatest risk of this is where

- Mobile app betting simulators: if you have to deposit money expect it to count as gambling even if it is technically not.

- Cash withdrawals: this is the most difficult and false assumptions on the purpose of your withdrawals could be an issue if it follows patterns that could be gambling related.

Can You Get a Car Loan with Gambling Transactions

All lenders have their own internal thresholds for an acceptable level of gambling. So there is no acceptable amount of gambling to ensure you can still get a car loan.

As long as you are only betting a small portion of your income and do not demonstrate any patterns of problem gambling, then you should be fine.

There is nothing wrong with a casual bet on the weekend if you can afford it.

However, the less you gamble the better your loan application will appear.

If you would like some guidance on your car loan eligibility, then speak to one of our expert car loan brokers by submitting an enquiry below.

How to Fix Bank Statements with Excessive Gambling Transactions

If you think your gambling expenses may prevent you from being approved for a car loan, then the good news is you can overcome this problem within 90 days.

However, your first priority must be to consider if you do have a genuine problem with gambling and if you need some help.

Contact the following government services for assistance:

- Assistance to overcome gambling addiction: gamblinghelponline.org.au

- Self-exclusion from betting services: https://www.betstop.gov.au/

If you are a casual punter and just want to improve the quality of your car loan application, then you can apply the following tips:

- Take a 90-day break from any form of betting. This is the best option and can also help you save a deposit to put towards your new car.

- If you still want to have a bet, set a budget that is a small percentage of your disposable income.

- Deposit your budget into your chosen betting account in one transaction.

If you only have one transaction per pay cycle that represents a small portion of your spending money this this presents a responsible money manager who also likes a bet.

Presenting a Responsible Budget Manager

At Gusto Finance, we speak to a lot of customers who have been declined by a larger lender.

When we look at their bank statements, they are littered with unnecessary gambling transactions.

Often due to a lack of awareness of how this will be perceived by a lender.

The risk of writing an unsuitable loan is significant for a lender, and they will not give you the benefit of the doubt.

This is a good thing. Problem gamblers should not be getting themselves into debt.

But if you are a recreational punter who can enjoy things in a responsible way, then you now know how to ensure that you present an accurate picture of how you manage your finances.

Gamble responsibly 🙂