Business owners have access to a different set of commercial lending structures compared to a regular car loan.

They are subject to less regulation which gives commercial lenders more flexibility in the solutions they provide, and the application processes.

For the borrower, there are also a range of tax advantages associated with the car finance and asset purchase that can help reduce the net cost of acquisition.

However, to access these loans you’ll need an ABN, a revenue generating business, and the financed vehicle to be mainly for business use.

In this article, we’ll summarise the full application process and show you how business car finance works from start to finish.

Key Takeaways: Business Car Finance

| Business Finance Eligibility | To qualify for business car finance, you need an ABN, and the vehicle must be used predominantly (more than 50%) for business purposes. |

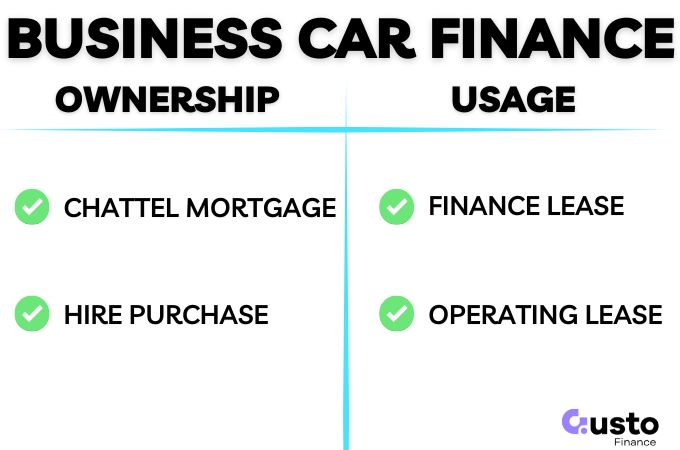

| Car Finance Structures | There are structures to support ownership (chattel mortgage and Hire Purchase) and usage (finance lease and operating lease). |

| Flexible and Fast Finance | Business finance is not subject to consumer regulations and is much more flexible than a regular car loan. Approvals can be secured in minutes in some cases. |

Business Car Finance Structures

There are multiple business finance structures that are generally split into two distinct categories depending on your end goal.

Asset Ownership Structures

These suit businesses building a balance sheet. You generally claim depreciation and interest deductions.

- Chattel Mortgage: You own the vehicle immediately. The lender holds a mortgage over the asset until the loan is paid.

- Hire Purchase: The lender owns the vehicle for the period of the agreement. You hire it for a fixed term and gain ownership automatically upon the final payment.

Asset Usage Structures

These prioritise flexibility and cash flow over asset accumulation. You essentially rent the vehicle for a fixed lease period.

- Finance Lease: You pay to rent the vehicle for the period of the leasing period, followed by a residual payment, or balloon, to take ownership at the end of the agreement.

- Operating Lease: You pay for usage of the asset and at the term’s end, you hand the vehicle back or upgrade to a new model.

Repayment Structures

All business car finance structures generally have a fixed repayment amount for the duration of the agreement.

The only variations to this are usually the last payment which could either be an adjusted amount to close out the agreement, or a larger residual payment.

If you use a balloon payment structure as part of your loan facility, or a residual as part of your lease, you may be up for a significant payment at the end of the term.

Does Vehicle Type Matter?

Generally speaking, the intended use of the vehicle is more important than the type of commercial vehicle.

The criteria is >50% business use for it to qualify for a business car loan.

Some categories such as vans, trucks, or buses are clearly for commercial use only.

However, passenger vehicles could potentially be subject to more scrutiny by the tax office as they are more suitable to personal use.

What Lenders Assess

Regardless of the finance structure, a lender’s evaluation will centre on two factors.

First is the asset being acquired. The vehicle’s type, age, and value can influence the type and cost of finance available.

For example, newer cars that will retain a strong resale value and deep secondary market are generally lower risk and the finance can be priced lower.

The second is the financial strength of the business entity and the repayment ability of its directors.

While this may sound labour intensive, there are actually plenty of low-doc car finance options that can be secured quickly and easily if some basic criteria are met.

The Chattel Mortgage: The Standard for Ownership

The Chattel Mortgage is the most recognisable finance structure for Australian businesses, and operates in a similar way to a regular car loan.

Quick Summary

The lender advances funds to the dealer to purchase the vehicle, and your business takes ownership immediately.

The lender registers a mortgage over the vehicle on the Personal Property Securities Register (PPSR) as security.

Once the final payment is made, this security interest is removed.

Terms of the Agreement

You lock in a fixed interest rate for the repayment term, which is over 1 to 7 years.

To manage cash flow, you can lower monthly repayments by:

- Paying a deposit: Reducing the principal at the start.

- Adding a balloon payment: Deferring a lump sum (e.g., 30% of the loan) to the end of the term.

Tax and Accounting Treatment

This is generally tax efficient option with the following benefits available:

- GST: GST-registered businesses may claim the GST on the purchase price as an Input Tax Credit on their next BAS.

- Deductions: You can generally claim interest payments and depreciation on the business-use portion of the vehicle.

However, always speak to an accountant to check your company’s specific circumstances.

Trade-Offs vs. Leasing

You have full control over the asset given that you own it from the start of the agreement.

Allowing you to modify the vehicle with trade accessories or sell it whenever you choose.

The asset and debt will sit on your balance sheet which can impact your debt-to-asset ratio, whereas operating leases often remain off-balance-sheet.

Comparing Business Car Lease Structures

While monthly payments may look comparable, the legal responsibilities under each agreement can differ significantly.

You should quantify any additional out of pocket expenses prior to entering the agreement so you know the full cost of ownership.

There are three primary differences between each type of business car lease.

- Ownership: The lender holds the title during the term for all three. You only gain title upon final payment (Hire Purchase) or by paying the residual (Finance Lease).

- Resale Risk: With an operating lease, the lender carries the risk of the car’s value dropping. With a finance lease, you cover the gap if the car sells for less than the residual.

- Maintenance: Operating leases often bundle tyres, registration, and servicing. Finance leases and Hire Purchases leave these costs to you.

Operating lease quotes can look higher because more of these costs are bundled together.

You should always compare the total cost over the full term, and not just the monthly payment figures.

When to Choose Leasing Over Ownership

Leasing beats ownership for businesses managing fleets or rapid upgrade cycles.

It allows you to outsource vehicle registration admin., and sometimes maintenance, to reduce the internal workload and smooth out cash flow.

Business Loan Tax Considerations

Tax outcomes depend entirely on your business entity, the income year, and your business-use percentage of the financed asset.

The following are general parameters to be aware of, but you must always confirm your specific strategy with a qualified accountant.

GST Credits

GST-registered businesses can typically claim input tax credits on the vehicle purchase price via their Business Activity Statement (BAS).

This often provides a significant cash flow injection shortly after purchase.

However, the claimable amount is strictly limited to the business-use percentage of the car.

If you use the vehicle 50% for personal trips, you can only claim 50% of the GST.

Additionally, the total GST credit is generally capped at one-eleventh of the car limit, regardless of the vehicle’s actual price.

The ATO Car Limit

Generally, businesses claim depreciation (decline in value) on the business-use portion of an asset over time.

However, for passenger vehicles, the ATO applies a strict ceiling known as the car limit.

The 2024–25 car limit was $69,674.

So, if you finance a luxury SUV for $90,000, you cannot depreciate the full purchase price. Your tax deduction is capped at $69,674. The remaining $20,326 creates no tax deduction benefit.

Luxury Car Tax (LCT) Thresholds

Vehicles with a GST-inclusive value exceeding the LCT threshold attract a tax of 33% on the dollar amount above the limit.

This increases the total loan amount required.

The 2024–25 thresholds were $91,387 (fuel-efficient) and $80,567 (other).

The significantly higher threshold for fuel-efficient cars (such as EVs and certain hybrids) is a government incentive to modernize fleets.

Simplified Depreciation and Instant Asset Write-Off

Simplified depreciation rules allow eligible small businesses to claim an immediate deduction rather than depreciating the asset over several years.

Because these thresholds change with federal budgets, you must verify the ATO guidance for the specific year the car is installed ready for use.

The car limit still applies.

Even if the instant asset write-off threshold is $150,000, your deduction for a passenger car remains capped at the car limit (e.g., $69,674).

You cannot write off the full cost of a luxury vehicle.

Business Car Finance Eligibility and Application Process

Asset finance is designed for speed. With the correct documentation, you can move from application to settlement in less than 24 hours, and often on the same day.

Processing time can vary significantly on a low-doc compared to a full-doc application. This is dependent on the complexity of the documentation provided.

While the criteria will vary by lender, you typically need:

- Entity Details: ABN, time trading, and proof of GST registration (usually 6-12+ months).

- Financial Evidence: Recent Business Activity Statements (BAS), bank statements, or a Profit & Loss.

- Vehicle Details: Dealer invoice or registration papers.

Low-Doc Pathways

A low doc application does not require detailed financial documentation and is the fast track to loan approval.

All you need is an ABN registration and your ID to qualify.

You can get a better deal if you also have a GST registration and own property, but it’s not mandatory to get an approval.

Frequently Asked Questions

Can I get a business car loan as a sole trader?

Yes, you do not need to be a PTY LTD company to qualify for business car finance. Sole traders and contractors are fully eligible as long as you have an active ABN and the vehicle will be used predominantly for business purposes.

Can I get business car finance with a brand-new ABN?

In some cases yes, but your options will be limited. You will either need to be a property owner, or work in trade that qualifies with specialty lenders. Your options increase after 6 months of trading history.

Do I have to be registered for GST to qualify?

No, GST registration is not mandatory to get a business car loan. However, you will be able to access a larger maximum loan amount if your business is registered. This will also unlock some of the tax benefits available with a business car loan.

Matching the Loan to the Business Needs

To determine what business car finance option works best you should first be clear on the use case for the vehicle, and the lifespan you need it for.

You should also consult with an accountant to determine the optimal tax structure for your situation.

From there, you need to find the best loan solution to match your objectives, that can be attained with the least amount of work.

Our team has access to over 50 lenders and can find the most suitable lender for you in seconds. So get in touch below to start a conversation.