A car loan will not always increase your car loan premium, but it will require you to maintain comprehensive coverage for the duration of the loan period.

This means that you cannot opt for narrower insurance policies that can save you money.

In this article, we will explain why a high level of coverage is mandatory and how to check if the cost increases based on the finance component.

Key Takeaways: Auto Finance Insurance Costs

| Mandatory Comprehensive Insurance | If you have a secured car loan, you must have Comprehensive Car Insurance to ensure the full value asset of the vehicle is covered. |

| Finance Loading in Premiums | Most major insurers do not charge extra just because you have a loan. Some smaller insurers do apply a risk loading, so shop around! |

| Interested Party | You must list your lender as the Interested Party or “Financier” on your policy. This ensures they get paid first in a total loss event. |

| Market Value Shortfall | A vehicle insured at market value may leave a shortfall between the loan amount and the insurance payout that the borrower is liable to pay. |

Mandatory Comprehensive Insurance

If you have a secured car loan, the lender holds a financial interest in the vehicle until the loan is repaid in full.

To protect the value of this asset, lenders mandate comprehensive insurance coverage for the entire loan term.

This covers all damage to your car plus third-party liability.

Cheaper alternatives, such as Compulsory Third Party (CTP) or Third Party Property insurance will not protect the secured asset.

You are also exposed to significant losses under these policies. Which is a big risk to take on such a costly asset.

Additional Contractual Obligations

Your car loan contract may have additional requirements when setting up your insurance policy.

Check for any specifications around the following items:

- Interested Party: You must usually list the lender as the financier or interested party on the Certificate of Currency. This ensures insurance payouts go to them first to clear the debt.

- Agreed Value: Some lenders may require Agreed Value policies to ensure the payout covers the full loan balance, but in most cases this is not required.

- Maximum Excess: Lenders may cap your voluntary excess (e.g., at $800 or $1,000) to ensure you can afford to make a claim if the car is damaged.

You also need to renew your policy each year.

While some lenders may not follow this up, if the vehicle is involved in an accident you could be left with a loan and no vehicle if you are not covered.

Does a Car Loan Increase Your Premium?

A car loan is not a universal surcharge on your insurance policy.

However, finance owing is a rating factor for some insurers, meaning the price can vary depending on who you choose.

Why Insurers Treat Loans Differently

Insurers rely on proprietary data to calculate risk, and their formulas differ significantly:

Some insurers may treat financed vehicles as higher risk. Their data may correlate borrowers with higher claim frequencies or specific driver demographics.

Others ignore finance status entirely. They price the policy purely on the driver, the vehicle, the postcode, and the cover selections.

The Real Drivers of Higher Costs

In practice, borrowers often face higher premiums due to mandatory lender requirements rather than the loan itself.

Lenders mandate comprehensive insurance, which prevents you from choosing cheaper third-party property cover.

Furthermore, borrowers often select a higher ‘Agreed Value’ to ensure the payout covers the entire loan balance in a total loss event.

This higher insured value increases the premium to avoid a financial shortfall.

How to Check for a Finance Loading

You can easily isolate this cost when comparing quotes online.

Fill out your quote details and keep every variable identical (car value, address, driver age). Then, simply toggle the finance owing option on and off.

If the price jumps, you have found an insurer that applies a specific loading. If it stays the same, that insurer rates purely on asset and driver risk.

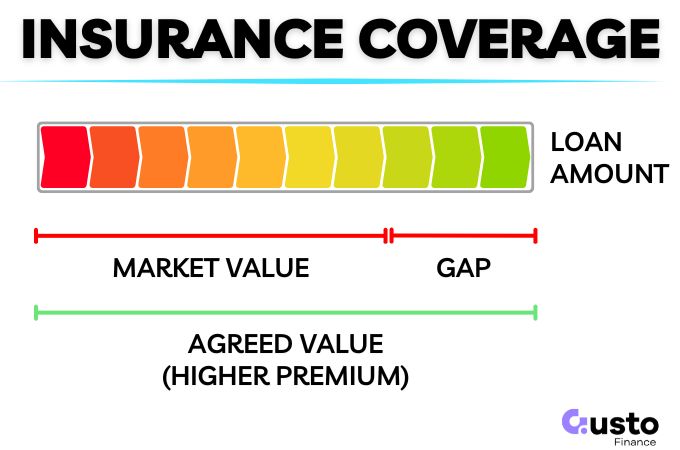

Agreed Value vs Market Value

There are two categories of asset valuation within your policy:

- Market Value: Pays what the car is worth at claim time. This figure drops as the car ages.

- Agreed Value: A fixed amount locked in at the start of the policy, regardless of depreciation.

In a perfect world your insurance coverage would be enough to cover the full loan balance.

However, the loan-to-value ratio is usually too high at the start of the loan repayment period for this to be possible.

Any increase in coverage to an agreed value will also push your premium costs up significantly.

The Loan Shortfall Risk

New cars depreciate faster than loan balances decrease, especially in the first two years.

If you insure for Market Value, a total loss could leave you thousands of dollars short in the event of an accident.

Agreed Value costs more, but it transfers some of that depreciation risk to the insurer.

But it all depends on how large the gap is, and whether the trade off in cost now vs future risk is worth it to you.

A lender will rarely look to enforce the higher level of coverage.

They will, however, expect you to pay the shortfall.

How to Set Your Insured Value

- Get quotes for both variations. If the premium difference is small, Agreed Value is the safer choice.

- If you have a small deposit or long loan term (5–7 years), you are at a higher risk of a shortfall. You could either choose Agreed Value or add GAP insurance.

You should also be careful not to over-insure when your policy comes up for renewal.

If you lower your Agreed Value annually to match your remaining loan balance you can save on premiums.

How to Lower Premiums

There are some steps you can take to minimise your premiums while retaining comprehensive coverage.

- Raise your voluntary excess to the lender’s maximum limit.

- Restrict coverage to named drivers over 25 years old.

- Include as much information as possible that may reduce the insurer’s risk (e.g. secure garage parking).

Often the best thing you can do is shop around.

The variance between insurers can be significant and you can avoid any insurer who increases the premium for a financed vehicle.

Frequently Asked Questions

Is car insurance always more expensive if you have a loan?

Not always. Some insurers factor finance status into their risk pricing, while others do not rate it at all. You can avoid the increased insurance cost by shopping around.

Do I have to tell my insurer the car is under finance?

Yes, you have a duty of disclosure to answer all questions accurately during the application. Your lender will usually require you to list them as an interested party on the Certificate of Currency.

If my car is written off, do I get the money or does the lender?

The insurer pays the lender first to ensure the payout is used to clear the debt on the secured asset. You will only receive funds if the insured amount exceeds your payout figure.

Can I switch to third-party property insurance after buying the car?

Generally, no. Most secured loan contracts mandate comprehensive insurance for the full term of the loan to protect the lender’s asset.

Minimise Your Insurance Costs

While the additional cost of comprehensive cover can be burdensome it also ensures you are not exposed to undue risk after taking out a substantial loan.

All you can do is make sure you are getting the cheapest policy possible while providing the require threshold of coverage.

Avoid insurers with premium loading for financed vehicles by shopping around.

You may be surprised by how much you can save with a little bit of effort.

If you would like a free consultation to work out your total cost of buying a new car, get in touch with the Gusto team below.