When acquiring new assets for your business, the finance structure you use can lead to vastly different outcomes with your cash flow and tax position.

Two of the most common products utilised are a chattel mortgage (secured loan), and a lease agreement (renting the asset).

Both have different obligations in terms of maintenance costs, the size of GST claims, and your overall cash expenses.

In this article, we will compare each product on a 7 key items to help you in identify what is most suitable to your business needs.

Key Takeaways:

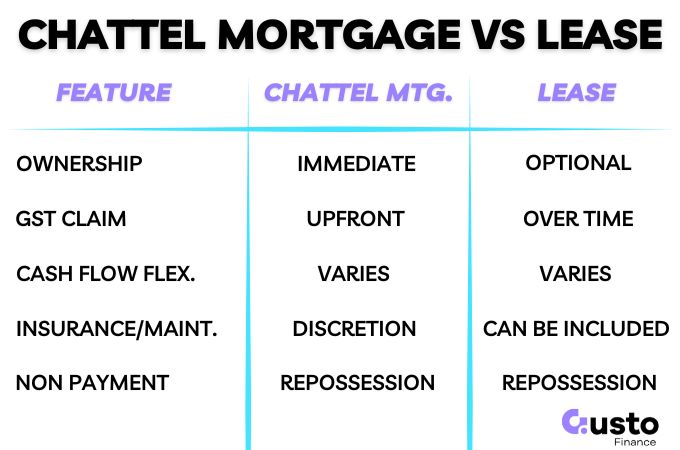

| Difference Between a Lease and a Loan | A Chattel Mortgage finances the purchase of the asset and the lender has a mortgage over it. A Finance Lease means the lender owns the car, and you rent it for a fixed term. |

| GST Credits | A Chattel Mortgage enables the full GST component to be claimed in your next BAS. With a Lease, you claim the GST progressively. |

| Tax Deductions | Under a Chattel Mortgage, you claim interest and depreciation. Under a Lease, you typically claim the full rental payment as an operating expense. |

| End of Term | Chattel Mortgages end when the loan is paid and security released. Leases offer the chance to purchase the asset, extend the term, or return it. |

Business Asset & Equipment Finance Options

There are a number of commercial finance options available to business owners is very different to standard consumer loans

Chattel Mortgage

A chattel mortgage is a business loan that is used to finance the acquisition of commercial assets.

The purchased asset is held as security over the loan until it is repaid.

At the end of the loan term, the encumbrance is removed, giving the business clear title of the asset.

Your business is considered the owner from day one for tax purposes, while the lender holds a mortgage over the asset as long as there is an amount owing.

Finance Lease

A finance lease operates like a long-term rental.

The financier purchases and owns the vehicle on your behalf, and your business pays for its use over a fixed term.

Some contracts will conclude with a pre-agreed lump sum payment, known as the residual value, if you wish to take possession of the vehicle.

This is different to a Hire Purchase agreement where the end goal is for ownership to transfer to the business.

A lease is intended to have an end date where the asset is returned by the business.

However, some finance lease agreements have an option to purchase, without the obligation to, once the agreement expires.

Chattel Mortgage vs Finance Lease: Detailed Comparison

Below we will compare these finance structures on 7 key points of difference.

Many of these will depend on your after tax benefit, and the how much flexibility you need longer term.

This is only high level information and seeking professional tax advice prior to committing to a lease or loan contract is needed.

However, the points below will give you a head start in understanding the concepts behind a lease compared to a chattel mortgage.

If you would like to discuss what options are available to your business get in touch with our expert team below.

1. Asset Ownership and Control

With a chattel mortgage, your business owns the vehicle from day one.

The lender registers a security interest, which is removed after the final payment. This structure gives you full control over the asset.

Under a finance lease, the financier remains the legal owner throughout the agreement.

You pay only for the right to use the vehicle.

This core distinction dictates who carries the resale risk and ultimately controls decisions about modifications, branding, and disposal.

2. How GST Treatment Impacts Your Cash Flow

A chattel mortgage usually allows the business to claim the vehicle’s entire GST component upfront in your next Business Activity Statement (BAS).

This delivers a significant cash injection for GST-registered businesses.

Under a finance lease, GST is included in each monthly rental payment.

You claim this credit back progressively over the agreement’s term.

If immediate cash flow is your priority, the chattel mortgage’s GST timing can be the deciding factor.

3. Comparing Tax Deductions

The primary tax difference between these options is what your business can claim.

Under a chattel mortgage, you typically claim deductions for loan interest and the vehicle’s depreciation.

This can be highly effective when accelerated depreciation incentives are in place for business, like the instant asset write-off.

With a finance lease, the entire rental payment is generally treated as a deductible expense, simplifying your claims.

The most tax-effective option depends on your business profitability and current ATO rules.

Model both scenarios with your accountant to make the correct financial choice for your situation.

4. Balance Sheet Impact and Future Borrowing

A lease creates a ‘right-of-use’ asset on the balance sheet, and a corresponding liability.

A chattel mortgage is more direct, appearing as an asset and a loan liability from the start.

Both financing structures impact your company’s leverage ratios which could become a factor for future borrowing.

If you plan to seek more equipment or fleet finance soon, you should discuss this with our team prior to committing to either a lease or a chattel mortgage.

5. The Final Payout

Whether there is a final payout depends entirely on how each structure is initially setup.

You can use a balloon payment as part of your chattel mortgage to keep your ongoing repayments down and preserve cash flow.

While this makes payments more affordable, it does introduce additional risk if you cannot make the final payment.

Or if your vehicle’s market value falls significantly through the repayment period and you cannot recoup sufficient value on sale or trade-in to cover the balloon.

A lease can also have a residual payment at the end of the rental period if the lessor wishes to purchase the asset outright.

This is one of multiple options for a lease at the end of the term.

6. End-of-Term Flexibility

At the end of the repayment term for a chattel mortgage the security is released by the lender, and the contract is complete.

If there is a balloon payment due this would either need to be paid, or refinanced into a new loan to repay this amount over time.

All very straight forward for a chattel mortgage.

A finance lease is much more flexible with three options often available at the end of the term:

- pay the residual value to take ownership,

- refinance that amount into a new loan,

- or return the vehicle.

This choice depends on your asset strategy. If you keep vehicles long-term, a chattel mortgage is more direct.

If you prefer to refresh your fleet regularly, a lease provides better flexibility.

7. Early Exit Penalties and Contract Flexibility

Both leases and chattel mortgages can involve significant payout figures and break costs if you sell or refinance early.

This is often overlooked by business owners when entering these contracts and can cause a nasty shock.

A contract you can’t exit cheaply is a major risk if your business is growing, seasonal, or uncertain.

Before signing any agreement, ask your financier for written confirmation on:

- The early termination fee schedule and payout calculation method.

- Procedures and costs if the asset is sold or written-off mid-term.

Does a Chattel or Mortgage Suit Your Business?

A lease and chattel mortgage have crucial distinctions in asset ownership, the timing of GST claims, and your options at the end of the term. The best choice for your business depends entirely on what you prioritise.

Use the points below to navigate directly to the comparison that matters most to you.

- If your main goal is asset ownership and maximising your upfront GST claim, focus on the ownership and taxation sections.

- If you value flexibility to upgrade vehicles regularly, the sections covering end-of-term options and early exit risk are more important.

Each topic below offers a direct comparison to help you decide.

Frequently Asked Questions

Are chattel mortgages and leases only for vehicles?

No. While common for vehicles, both business finance structures are commonly used for a broad range of business assets. Such as vehicles, equipment, technology, and machinery, subject to lender criteria.

Can I claim GST on a chattel mortgage and a lease?

Yes, GST-registered businesses can claim GST credits on both. However, the timing is very different. If buying the asset the full GST can usually be claimed in the next BAS, if leasing it can only be claimed on payments made in that quarter.

Which is usually better for a small business?

A chattel mortgage often suits a GST-registered business buying a core asset (like a ute) for long-term use. A finance lease can better suit a businesses that upgrades their fleet every 2–3 years and need flexibility over ownership.

Comparing the True Cost of Finance

To compare commercial finance deals accurately, you must calculate the true cost that accounts for the tax benefits of each option.

This is the sum of your total repayments, the final balloon or residual payment, and all establishment fees.

Depreciation, GST credits, and overall tax deductions also need to be considered.

These calculations depend on the type of asset you wish to acquire, the finance structure, and your tax situation.

You will need a qualified accountant to help you work through a scenario relevant to your business.

Our team of expert brokers can conduct a preliminary assessment so you know what products you are eligible for, and the costs involved.

Click below to get started.