As a business owner, having access to fast vehicle finance without a ton of paperwork is important.

Low-doc car loans can go from application to approval in minutes, and with little more than an ABN registration and your ID.

However, a lender is still going to run a credit check on you.

If your score is low then you may have to go down a more difficult pathway.

In this article, we will discuss what credit score you need to qualify for a low-doc car loan, and what happens if you fall short.

Key Takeaways: Low-Doc Credit Score

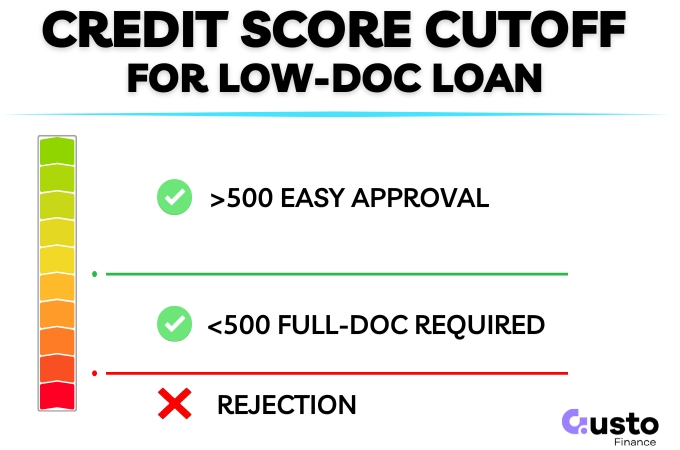

| Current Credit Score Threshold | A credit score of 500+ is generally the gateway to a fast Low Doc approval, depending on the lender. |

| Below a 500 Score? | You can still get approved but more documentation will be required to assess if you can repay the loan. |

| Protect Your Credit Score | Don’t spray and pray with applications. A formal decline hurts your score further. Use a broker to check eligibility with a soft check first. |

Achieving Fast Low-Doc Approval

Credit risk is usually a broad spectrum with a range of contributing factors.

But with a low-doc commercial loan, there is a fast track if you can tick just a couple of boxes.

- ABN at least 6 months since registration.

- Is a property owner.

The second point strengthens an application and almost guarantees approval, but is not always needed.

GST registration will also strengthen an application and increase the potential borrowing capacity, but is not always necessary for a smaller approval.

That is a total of just two documents plus an ID to be approved for a low-doc loan in just minutes.

In those few minutes, a lender will run a credit check to ensure there are no major red flags. The first being a low credit score.

Minimum Credit Score for a Low-Doc Loan

As long as your credit score is above 500 then you can remain on the fast track to approval.

Even if you are not a property owner.

Your interest rate is also likely to be comparable to some of the cheaper consumer car loans on the market.

It is a great deal for business owners and the self employed, who can access a great rate with minimal time investment.

However, if you have had credit problems in the past and your score is below this benchmark, lenders see higher risk and will have to investigate further.

This means more paperwork required, fewer lender options, higher interest rates, and potentially stricter conditions (like a larger deposit to offset that risk).

To find out if you qualify without damaging your credit score, click below to get in touch with the team.

What Happens If My Credit is Below the Threshold?

Some lenders will consider a commercial car loan below the 500 threshold, but more documents will be required.

They do this to confirm the financial stability of the business when the score indicates there could be a problem.

A higher score reduces paperwork scrutiny, a lower one invites it.

At this point, it is no longer a low-doc loan. Some, probably not all, of the following documents could be requested:

- Proof of property ownership (e.g. a rates notice)

- Business Activity Statements

- Up to 6 months of business financials (bank statements)

- Tax returns (up to two years)

- Accountant’s letter

- Evidence of cash to be used for a deposit

The list of required documents will be determined by the specific lender.

How to Strengthen a Borderline Score for Approval

A borderline credit score may not mean automatic rejection, but you will need a good broker advocating on your behalf.

Sometimes a lender can be flexible if there are special circumstances around the events that damaged your credit file in the first place.

However , this is no certainty and is a the discretion of the lender.

It helps if your credit score has been on the improve, and any other loans have been impeccably managed for some time.

It is also important to make sure you are applying at the best low-doc lender who may consider your unique circumstances.

Frequently Asked Questions

Is a 500 credit score a guarantee of approval?

A credit score alone does not guarantee approval. Lenders still assess your ABN trading history, and the vehicle itself. It unlocks a simpler process for your low doc car loan but doesn’t ensure final approval.

Can I get a low-doc loan with a score under 500?

You can still get a loan, but more documents are going to be required (e.g. bank statements) and perhaps some additional approval conditions (e.g. a larger deposit).

Can I get low-doc finance with a paid default?

Sometimes yes, but it depends on how long ago the default was and the current impact on your credit score. Some lenders are more concerned with recent or unpaid defaults which signal ongoing financial difficulty.

Does a car loan application hurt my credit score?

Your score can drop temporarily when a formal application is made and a credit enquiry lodged on your credit report. To protect your file, use a broker who can match you to the right lender without lodging multiple applications.

Securing Your Low Doc Loan

The criteria is very simple for low-doc loans, but the credit score element of your application is critical.

A score of 500 very attainable for most people unless you are in significant financial difficulty, or have mismanaged credit in the past.

Until these issues are resolved and your credit score is at least improving, then more credit may not be the answer anyway.

If you would like to speak to our expert team, get a quick eligibility check below (with no damage to your credit file).