If you run your own business you have the freedom to choose whether you take out a car loan in your own name, or through the business.

Your choice is likely to be most influenced by your tax situation, and which option is most accessible.

Chattel mortgages can be fast and easy to attain through your business with a decent trading history, and sound credit.

However, if you are also using the vehicle for personal use you may not qualify.

In this article, we will compare a personal car loan and commercial car finance so you can choose what is best for you.

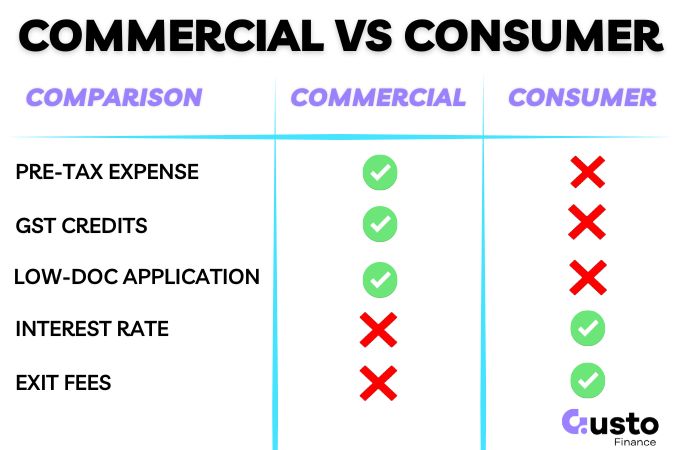

Key Takeaways: Business or Personal Car Loan

| Loan Eligibility | A Chattel Mortgage is exclusively for business owners (ABN holders) using the vehicle >50% for business. A Personal Car Loan is for individuals or business owners with <50% business use. |

| GST Credit | GST registered businesses may be able to claim the GST on the vehicle’s purchase price as an input tax credit in their next BAS. |

| Other Tax Differences | A consumer loan is paid with after tax income, and any business use is a deductable expense. Business loan costs are paid from pre-tax revenue. |

| Total Loan Costs | Interest rates and fees are comparable depending on your credit profile. However, commercial car loans have a much higher exit fee if you wish to repay the loan early. |

Understanding Each Loan Category

Chattel Mortgage

A chattel mortgage is business vehicle finance where your ABN-holding entity owns the car, and the lender takes a security interest over it.

It’s suitable for sole traders and companies using the vehicle for over 50% business-related travel.

Consumer Car Loan

A personal car loan is finance taken by an individual for primarily personal or domestic use.

For an ABN holder, it’s the better choice if business use is under 50% or you are not GST-registered and prefer simpler compliance.

This structure also provides consumer protections under the National Credit Code.

Eligibility Factors That May Decide Your Loan Type For You

You may have less choice than you think depending on the following two factors:

Factor 1: The 50% Business Use Test

A chattel mortgage requires the vehicle to be used predominantly for business.

Meaning over 50% of its use is for generating income. If the car is mainly for personal use, a consumer car loan is the appropriate choice.

Factor 2: How You Pay Yourself

A business car loan is reliant on the operating history of the entity.

Whereas a consumer car loan will consider your take home salary. Something that many business owners seek to minimise.

A small salary on paper will make it difficult to evidence enough income to service a car loan.

Chattel Mortgage vs Car Loan: Detailed Comparison

We have completed the comparison based on factors that are often different between each car loan category.

Any items that are the same have been excluded from the summary, these include:

- Maximum loan terms (up to 7 years acceptable for both).

- Fixed and variable interest rates available.

- Optional balloon payments in loan structure.

Tax & Cash Flow

Owning a car through a business entity is generally the most beneficial structure. However, you should always seek professional tax advice first.

The key difference between a business car loan, and a personal loan is that

- Expenses are paid from revenue, which is pre-tax.

- GST registered businesses may be able to claim the GST on the vehicle’s purchase price as an input tax credit. On a $55,000 vehicle with roughly $5,000 in GST, could mean a $5,000 claim on your next BAS.

- Loan interest and depreciation can also be deducted as an expense.

- Instant asset write off incentives have also been used in the past which can be hugely beneficial.

A consumer car loan is paid with your after tax dollars.

If you use the vehicle for the business you could claim a portion of the expenses against your taxable income, in line with the proportion used for business purposes.

You will need to keep detailed records to justify this though.

Application Process and Timeframes

Consumer car loan applications can be very thorough and arduous. This is due to the Responsible Lending regulations that all lenders must adhere to.

This is why your credit file and financials are looked at thoroughly. Which also means it can take longer.

Commercial car loans are not subject to the same regulations and lenders generally act to manage their own risk rather than meet a legislative requirement.

As a result, there is a lot more flexibility and discretion possible in the application process.

The lowest friction being the low-doc car loan.

You could be approved with as little as your ABN registration and ID, and in just a few minutes.

Loan Costs

The difference in interest rates for a consumer car loan vs a commercial car loan are comparable for high quality customers.

Auto finance lenders generally price based on their risk assessment and there are so many variables in this decision that it is difficult to present a direct comparison on rate.

The lowest interest rates achievable are likely to be in the 6% to 8% range for a good credit profile for each loan category.

Where the two can diverge is in the fee structure.

Both will attract an establishment fee, and depending on credit quality, a risk fee could also be added.

Whereas the exit fee on commercial car finance can be much more substantial.

Often in the thousands of dollars!

When compared to a personal car loan may only charge a few hundred dollars to exit a loan contract early.

Repayment Timing

A consumer car loan will have a set repayment schedule that can either be weekly, fortnightly, or monthly.

This will usually align with the borrowers pay cycle and will be a set and forget repayment plan for the life of the loan.

Commercial loans can be more flexible. Some unsecured loans can have daily repayments or other variations based on the business needs.

However, most car loans also adhere to the weekly, fortnightly, or monthly repayment schedule.

Is a Business Loan or Consumer Loan Best for You?

For GST-registered businesses using a vehicle over 50% for work, a chattel mortgage is usually the most tax-efficient choice.

It also requires the least amount of work to gain approval, which frees up your time to focus on your business rather than gathering paperwork.

While this form of financing is mostly unregulated, it is in the interest of a reputable lender to treat their customers fairly regardless of a legal obligation.

For mixed use, personal auto finance may be required and you’ll need to keep detailed records to ensure you are optimising tax deductions.

Just make sure your take home salary is sufficient to cover the loan repayments in addition to your other living expenses.

Ready to find the right loan structure? Get a fast, transparent comparison across our network of 40+ lenders.