If your employer offers access to a novated lease then the promise of paying for a vehicle with pre-tax dollars is very tempting.

But also confusing!

Is this any different from a car loan? And is it really cheaper?

Well, the answer is that it depends on your personal circumstances.

In this article, we will conduct a detailed comparison on both auto finance products so you can make a more informed choice.

Key Takeaways: Novated Lease vs Loan

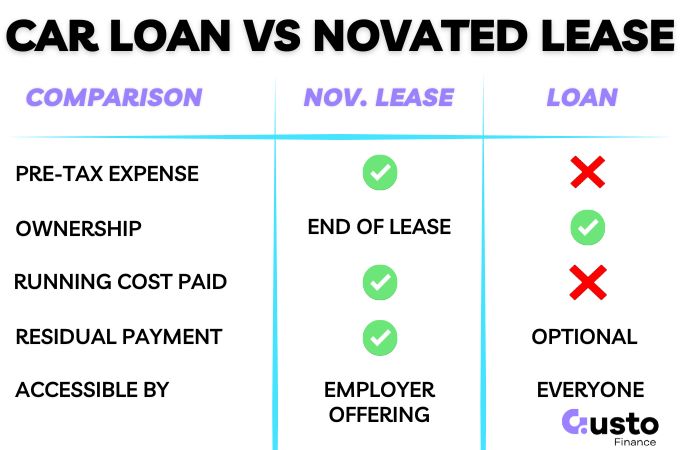

| Product Accessibility | Novated Leases are only for employees whose company offers salary packaging. Car Loans are accessible by everyone. |

| Tax Savings | Novated Leases use pre-tax salary, lowering your taxable income and saving you money on tax. Consumer car loans use after-tax income. |

| Ownership Status | With a Car Loan, you own the car from Day 1. A Novated Lease requires a Residual payment at the end of lease to keep the car. |

| Job Stability Risk | If you quit your job or get fired, the Novated Lease obligation transfers to you immediately. A car loan is not linked to your employer at all. |

Product Definitions

To compare a car loan and a novated lease, you must first understand their structure.

They are not just different ways to pay for a car; they are fundamentally different financial products.

What is a Novated Lease?

A novated lease is a three-way agreement between you, your employer, and a leasing company.

Your employer makes payments directly from your salary, often using pre-tax dollars for maximum benefit.

A fully maintained lease bundles all running costs into this single payment. The leasing company owns the vehicle, so you are renting it for the agreed term.

What is a Car Loan?

A car loan is a direct finance agreement between you and a lender.

You borrow a fixed amount to buy a car and make regular repayments from your after-tax income.

You own the car from day one, though the lender holds a security interest, meaning they can reclaim it if you fail to pay.

All running costs are your separate responsibility.

Two Terms That Shape Every Comparison

To compare any deal fairly, you must understand two concepts that control the total cost:

- Residual Value: This is a mandatory lump sum paid at the end of a novated lease to take ownership of the vehicle.

- Running Costs: These include all everyday car ownership expenses, like fuel or EV charging, registration, insurance, servicing, and new tyres.

Novated Lease vs Car Loan: 8 Point Comparison

1. Eligibility: Who Can Access Each Option

One of the biggest differences between a car loan and a novated lease is access to the product.

A novated lease is a workplace benefit available only to PAYG (Pay As You Go) employees whose company offers salary packaging.

Your payroll department manages the payments, creating a direct link between your job and your car finance.

If your employer doesn’t support novation, or you change jobs to a company that doesn’t, the arrangement must be restructured.

A car loan is available to almost anyone who meets a lender’s income and credit criteria.

This includes full-time staff, casual workers, contractors, and self-employed ABN holders.

The finance agreement is strictly between you and the lender, completely independent of your employment situation.

This makes your choice clear:

- Novated leases suit employees with stable employment at a company that actively supports the program.

- Car loans suit anyone without access to salary packaging, including self-employed workers, or those who prefer an agreement with no employer involvement.

If your company doesn’t offer novated leasing then your decision tree ends here.

Click below to get in touch with our team of brokers who can find you the best deal on a car loan for your circumstances.

2. Ownership and End-of-Term Decisions

A car loan and a novated lease treat ownership differently, creating a big decision at the end of your term.

With a standard car loan, you own the vehicle from the start.

After your final repayment, the car is 100% yours with no further obligations.

Under a novated lease, the finance company owns the car for the duration of the lease term.

At the end of the term, you must pay a residual amount to take ownership of the vehicle.

You have three options to deal with this payment:

- Pay the residual and take full ownership of the car.

- Refinance the residual amount into a car loan.

- Sell or trade in the vehicle to pay the residual and start a new lease.

This structure creates a clear trade-off.

A novated lease offers lower ongoing payments but requires a significant financial decision later, suiting those who upgrade cars frequently.

A car loan is better for buyers seeking long-term ownership without a forced end-of-term decision.

Although you can still opt-in to a balloon payment structure if you want to minimise your ongoing repayments.

Residual percentages are structured according to ATO guidelines, so always confirm the exact figure with your provider.

3. Cost of Ownership

Advertised weekly repayments are designed to look affordable, but they often hide the full financial story.

A low weekly figure might conceal high fees, a large final balloon payment, or ignore running costs altogether.

To truly compare a car loan and a novated lease, you must calculate the Total Cost of Ownership (TCO).

For an accurate calculation you will have to be clear on what is, and what is not, included in your lease contract.

Servicing and maintenance of a vehicle is a significant expense and can change the outcome of the comparison significanlty.

To get a clear picture, follow these steps for each quote:

- Calculate total repayments: Multiply your regular payment by the number of payments over the full term.

- Include all fees: Add any establishment fees, ongoing administration fees, or other charges listed in the contract.

- Factor in running costs: For a car loan, add your estimated total for fuel, insurance, registration, and servicing. For a lease, confirm these are realistically budgeted within your repayments.

- Add the final payment: Include the residual or balloon amount required to take ownership of the car at the end of the term.

- Adjust for tax impact: For a novated lease, subtract the estimated income tax saving from the total. This converts the cost to an after-tax figure that can be fairly compared to a car loan.

Here is an example calculation that compares a $40,000 car over a 5-year term with estimated running costs of $5,000 per year.

The novated lease bundles these costs into the lease payment, and the car loan does not.

| Line Item | Car Loan (After-Tax) | Novated Lease (Pre-Tax) |

|---|---|---|

| Vehicle Loan/Lease | $40,000 | $40,000 |

| Finance Repayments | $47,522 | $60,000 |

| Ongoing Fees | $1,000 | $1,500 |

| Running Costs | $20,000 | Included |

| Residual Payment | – | $11,252 |

| Tax Impact | – | -$10,000 |

| Estimated 5 Year Cost (TCO) | $68,522 | $62,752 |

The above example is for a regular vehicle that runs on petrol. EVs can have various tax exemptions that can alter the TCO.

4. Running Costs: Bundled Expenses vs. Pay-As-You-Go

A key feature of a novated lease is the fully maintained package.

This means your single payment bundles estimated costs for fuel, insurance, registration, servicing, and tyres for predictable, set-and-forget budgeting.

With a car loan, you manage these running costs yourself.

You pay each bill as it comes from your bank account, giving you freedom to shop around for the cheapest insurance or your preferred mechanic.

If you put in the effort to shop around you can save a lot of money on these items of the course of a car loan repayment term.

The trade-off is convenience versus cost.

While bundling simplifies budgeting, the running cost estimates can be inflated.

A lease provider’s packaged insurance or tyres may also be pricier than what you could find independently, eroding potential savings.

A novated lease would best suit those who value stability in cashflow and want to avoid juggling multiple car-related bills.

Whereas a car loan may be preferred by someone wanting total control over expenses, drives low kilometres, or are confident they can find better deals on their own.

Before signing, ask the lease provider for a line-by-line running cost budget.

Compare it against your actual spending from the last 12 months to see if the convenience is worth the cost.

5. Tax Benefits: Key Selling Point of a Novated Lease

The primary advantage of a novated lease is the potential for tax savings.

This is possible because payments are made from your pre-tax salary through a process called salary packaging.

By paying for the car and its running costs before income tax is calculated, you lower your total taxable income.

This means you pay less tax, reducing the vehicle’s overall cost.

For eligible electric vehicles (EVs), this benefit can be even more substantial.

At the time of writing, government policy allows Fringe Benefits Tax (FBT) to be reduced or removed entirely.

Eligibility depends on the vehicle’s value and the specific legislation at the time.

These savings are not automatic.

The final financial benefit depends directly on your income tax bracket, the specific structure of the lease, and whether the vehicle qualifies.

The higher your marginal rate of tax, the better off you will be under a novated lease.

However, you should always seek advice from a tax professional before committing to a contract.

6. Changing Employment

A novated lease is tied to your employer. While you are employed, payments are seamless through payroll deductions.

If you leave your job, the full financial responsibility transfers directly to you until you re-novate it with a new employer, pay out the contract, or sell the vehicle.

A car loan is independent of your job.

The agreement is between you and the lender, so your repayment obligations remain the same if you change employers.

This offers greater stability during career transitions.

7. Flexibility for Upgrades and Early Payouts

Your ability to pay off debt early or upgrade your car ahead of schedule depends on your finance structure.

A car loan offers maximum control.

You can make extra repayments to pay it off faster, saving on interest.

You can also sell the vehicle anytime by getting a payout figure from your lender and settling the remaining balance.

This gives you the freedom to adapt as your financial situation changes.

A novated lease is more rigid. It is a fixed-term agreement, and ending it early means breaking the contract.

This triggers significant payout costs based on remaining payments and the car’s market value, plus administration fees.

These costs can easily outweigh the initial tax savings.

8. Car Loan Eligibility

A cost comparison between a car loan and a novated lease would be influenced most by the interest rate you qualify for in a car loan.

Auto lenders price for risk and the variance can be significant.

We write loans anywhere from in the 5%-7% range, all the way up to the high 20% for those with bad credit.

The type of vehicle, age, KMs on the clock, and where you buy it all influence your interest rate.

And you always have to weigh this up with the chances of being approved for the car loan at all.

You can get a free assessment of your options in minutes by contacting our team below, saving you the legwork of shopping around.

Frequently Asked Questions

Can I get a novated lease if my employer doesn’t offer one?

No you can’t. It’s an employer-sponsored benefit that requires your company to manage salary deductions.

What happens if I change jobs mid-lease?

You become responsible for all payments until you can arrange a new novation with your next employer.

Do novated leases always save money?

Not always. Savings depend on your tax bracket, vehicle, and provider fees. Always compare the total cost against a car loan.

What is a residual and do I have to pay it?

A mandatory lump-sum payment at the lease end. You must pay it to own the car, refinance it, or sell the vehicle to cover the cost.

Who is Most Suitable for a Car Loan or Lease?

The best choice hinges on your employment, ownership goals, and the Total Cost of Ownership (TCO).

A novated lease uses pre-tax income for potential tax savings, while a car loan offers straightforward ownership and control.

Always compare direct quotes, not just the advertised weekly payments.

A novated lease suits employees with access to salary packaging, especially high-income earners or those buying an eligible EV.

Using pre-tax income for the car and its running costs can lower your TCO.

This benefit depends on realistic cost budgets and your comfort with job-change risks and the final residual payment.

A secured car loan is best if you are in a lower tax bracket, are likely to move jobs within the lease period, or just don’t have access to salary packaging.

You own the car immediately, the finance is independent of your job, and you control all running costs.