To determine the best car loan term for your circumstances you need to balance affordability, total cost, and what loan products you are eligible for in the market.

You can prepare yourself for this by fully understanding the relationship between a monthly repayment amount, interest rates, and time.

In this article, we will discuss the most important variables that determine your loan term and show examples of how they change over different timeframes.

Key Takeaways:

| Cost vs Repayment Trade-Off | A longer term means lower monthly repayments but significantly higher total interest costs. The opposite is true for a short loan term. |

| Borrowing Power | The longer the loan term the higher you maximum loan amount, and the higher priced car you can afford. |

| Lender Limits on Older Cars | Not all lenders offer 7-year terms. Some may cap older used car loan terms at 3–5 years, which can limit your options. |

| Refinancing Strategy | You can start with a 7-year term to keep payments low, then make extra repayments or refinance later to pay it off faster and save on interest. |

Car Loan Repayment Term Ranges

The most common repayment term on a car loan ranges from three to seven years.

While it may sound optimal to repay the loan in the shortest possible timeframe, there will be significant variation in the size of your repayments.

As a result, the size of the loan you can manage will also vary significantly depending on your loan term.

For example, if you borrow $30,000 at 10% interest to buy a car your repayments can vary but almost 100%:

- 3 year term: $968 per month

- 7 year term:$498 per month

If you can afford the higher repayment then great! You can repay your loan much faster.

For many, the longer term is a necessity rather than a preference.

This is just one example of what could determine the appropriate loan term.

5 Factors That Will Limit Your Loan Term

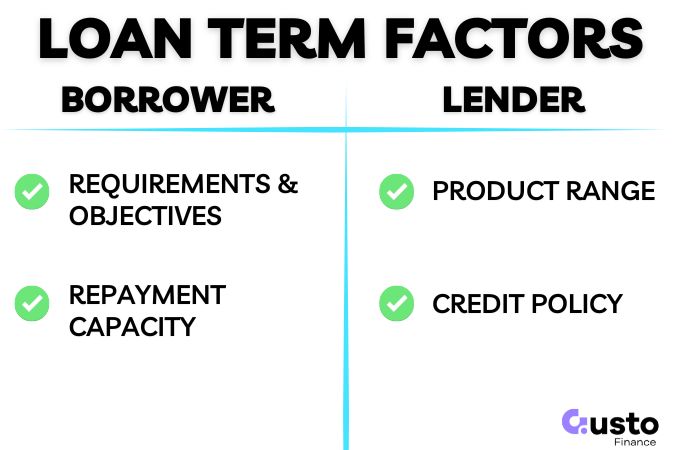

There are factors on both the borrower and the lender’s side that will impose a limit on the loan term.

A quick summary of the factors on each side is:

- Borrower: How much do you want and how much can you afford with a set timeframe.

- Lender: What loans do they offer, and are they willing to lend the money to you.

A loan will eventuate when there is sufficient overlap between the two parties.

If you would like a no obligation preliminary assessment of what you could borrow, over what timeframe, then get in touch with our expert team below.

1. Your Requirements & Objectives

Lenders must ensure that any loan aligns with your requirements and objectives, as part of responsible lending obligations.

This is why in every loan application you must nominate an amount you would like to borrow.

A lender cannot offer you more credit than you have applied for, even if you can afford it.

They can, however, adjust the amount down as long as the revised amount still meets your requirements & objectives.

This important because the loan amount is one of the biggest factors in determining the repayment term.

2. How Much You Can Afford

As we have seen in the earlier example, your repayments can vary significantly based on the repayment term.

So if you have stated that you want a $30,000 loan and can only afford a $500 a month repayment then you can only be expected to repay this over 7 years.

You simply cannot afford to commit to a shorter loan term.

3. Lender’s Product Range

Continuing with the same example, what if the lender you have applied with only offers a maximum of 5 year loan terms?

You would not be able to service the loan and would either be declined or offered a lower amount you can repay within the maximum loan term.

For example, you apply for $30,000 but the most you can possibly repay with your $500 a month repayment capacity is $23,500.

You still get a loan offer, but it is capped at the five year period even if your preference was a larger loan over 7 years.

4. Credit History

The longer the loan term the higher chance of something going wrong. Therefore, a lender may restrict loan terms for those who have bad credit.

While you can still secure finance in many cases. You will attract a higher interest rate, be limited to a lower borrowing amount, and a shorter loan term.

This is so the lender can reduce the risk of making such a loan.

5. Age of Vehicle

Some older cars may be capped at a 3-5 year loan term.

In most cases, a lender will assess the vehicle’s eligibility to be held as security based on the age at the END of the loan term. Not at the time of purchase.

As a result, 7 year loan terms will be harder to secure once a car is more than 7-8 years old.

Short-Term vs Long-Term Car Loan Examples

Repayment Amount & Cost

Now let’s look at some more detailed comparisons of repayment amounts and the total cost of a short term vs a long term car loan.

You can save a significant amount of money by repaying a loan faster but there is an opportunity cost to doing so, if you can afford it at all.

The two major variables are:

- Your repayment amount; and,

- Total cost over the life of the loan.

Not only does the three year loan term get you out of debt faster, but you save $6,986 in costs when compared to the 7 year loan term.

| $30k @10% | 3 Years | 4 Years | 5 Years | 7 Years |

|---|---|---|---|---|

| Repayment | $968 | $760 | $637 | $498 |

| Total Cost | $4,848 | $6,522 | $8,244 | $11,834 |

Borrowing Limit

Now lets look at how the maximum loan amount can vary if your repayment capacity is fixed.

The longer you have to repay the loan, the more you can borrow.

As discussed, whether these terms are possible will depend on your credit score and what products you are eligible for.

| $500 Max. Repayment @10% | 3 Years | 4 Years | 5 Years | 7 Years |

|---|---|---|---|---|

| Repayment | $498 | $499 | $499 | $498 |

| Max. Loan | $15,450 | $19,700 | $23,500 | $30,000 |

How to Determine The Best Car Loan Term For You

To put these examples into practical steps, you can take one of two approaches:

- Determine what you would like to borrow and calculate the shortest time period you can afford to repay the loan. Or,

- Calculate your maximum repayment amount, and use this to determine the maximum loan you need to buy the vehicle you want.

You can either use our repayment calculator for this, or just get in touch with our expert team below and we can do it for you.

Choose the Best Car Loan Term for You

Now that you know how the numbers work you can be more intentional with the car loan term you want to apply for.

If you expect your situation to improve over time then you can start with the longest repayment term available to you and make additional repayments as your budget increases.

Allowing you to start your car buying journey today with a clear idea of what is possible.

As always, if you need help with the numbers then get in touch with the team at Gusto.