A secured business loan will hold a specific asset as collateral, so if the borrower defaults the lender can take possession of that asset.

In comparison, an unsecured loan may sound like it would offer more protection for the borrower.

But this is usually not the case.

There are alternative mechanisms that lenders use when providing business finance that ensures their interests are protected.

So, what is the real trade off between a secured and unsecured business loan?

In this article, we will discuss how they really differ and what a business owner should pay attention to when organising their finance.

Key Takeaways: Unsecured vs Secured Business Loans

| Collateral Requirements | Secured loans are backed by a physical asset registered on the PPSR. Unsecured loans do not require a specific asset to be pledged upfront. |

| Liability for Unsecured Finance | Almost all Australian commercial lenders will still require a Director’s Guarantee, making you personally liable for an unsecured debt. |

| Cost & Limits | Secured loans offer lower interest rates and much higher borrowing limits. Unsecured loans carry higher rates and are usually capped between $500k and $1M. |

| Primary Use of Funds | Use an unsecured loan for fast, short-term cash flow gaps. Use a secured loan for long-term assets where you want the lowest possible interest rate. |

Comparison of Secured and Unsecured Business Loans

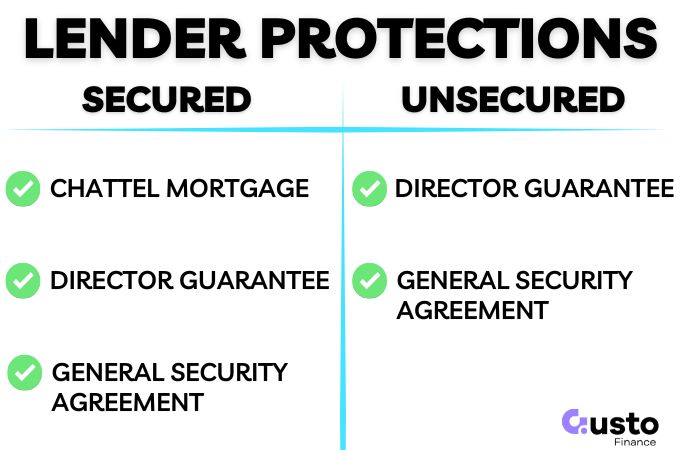

1. Lender Protections (and Collateral)

A secured loan will define the asset that is linked to the loan facility, and a security interest is registered on the Personal Properties Security Index (PPSR) until repaid.

If the borrower defaults, the lender can take possession of the security to recover the funds outstanding.

The security could be a physical asset like vehicles and equipment, or financial assets like receivables or purchase orders.

An unsecured loan might not demand specific collateral upfront, but lenders still protect their money using other legal mechanisms.

These can include:

- Director Guarantees: Personal liability if your business cannot repay the debt which can lead to lenders making a claim on privately held assets.

- General Security Agreement (GSA) or All Present and After-Acquired Property (AllPAP): Creates a blanket claim over all business assets

Not all of these mechanisms will be used in every unsecured business loan.

The lender protections used will depend on the borrower profile, lender policies, and amount being borrowed.

2. Cost of Secured and Unsecured Business Loans

Lenders price loans on risk. Pledging an asset reduces lender exposure, which typically results in lower pricing.

The higher risk of an unsecured loan is priced into your interest rate and fee structure.

A common blind spot in commercial lending is that there is no headline rate to use as a benchmark.

Lenders will usually only disclose a rate after they have conducted a thorough credit assessment.

The total cost of borrowing for both types of business loan will include:

- Rate type (fixed or variable)

- Upfront establishment fees

- Ongoing monthly charges

- Early payout rules (break fees can be high)

Secured finance rates can start around the 5%-6% mark, and run all the way up into the 30%+ range depending on the borrower.

Whereas unsecured loans can also start low, but run much higher.

3. Borrowing Limits

Secured loan limits are directly tied to the physical value and quality of your asset.

Lenders confidently offer higher amounts when commercial equipment or vehicles back the debt.

Unsecured limits rely entirely on your cash flow, credit profile, and total time in business.

Without physical collateral to offset the risk, these approved amounts are typically capped at somewhere between $500k and $1 million for a maximum loan amount.

While this sounds high, a secured loan for equipment can easily run into the millions of dollars.

4. Loan Terms and Daily Cash Flow

A low interest rate over a short repayment term could still place a large burden on your cash flow.

Unsecured finance typically demands a much shorter repayment schedule.

However, some lenders may consider a 5 year repayment term depending on your business profile.

Secured loans generally offer longer terms that align with the expected lifespan of the physical asset.

Allowing you to potentially spread the balance out over a longer period of time.

But again, this is entirely dependent on your business profile.

5. Settlement Speed and the Application Process

Unsecured business loans can be fast to process and can be a great option when there is an urgent need for a cash injection.

Secured finance can be a better outcome overall if you have the time, and upfront cost, that is required for asset valuations to be completed.

Lenders must verify asset condition, complete PPSR checks, and confirm insurance policies before drafting loan documents.

However, the speed also depends on the purpose of the loan.

A low-doc secured car loan can be approved in minutes if placed with the right lender!

Whereas more complex equipment, or financial assets that require more careful valuation, will take longer.

There is also variability in unsecured loan approval times that depend entirely on preparation and being placed with a compatible lender.

Messy bank statements, incomplete information, or a lack of transparency on business financials will lead to back-and-forth questions and delay a lender decision.

Clean documentation improves the chances of a fast settlement so you can get back to business.

6. Recovery Action if You Cannot Repay the Loan

Missing a repayment will trigger consequences for both secured and unsecured loans, but the immediate steps will vary.

Both loan categories will have implications for the credit profile of the directors and the business.

It is the recovery process where action will differ.

With a secured loan, the lender can repossess your pledged collateral without much notice.

A major risk here is operational. Losing the vehicle or equipment you need to trade can instantly halt your business and be very damaging.

Unsecured loans lack a specific asset pledge, but defaulting can lead to legal action directed at business and personal assets.

7. Sources of Funding

While the larger banks offer the sharpest pricing on commercial lending, they are very strict in their criteria and will often avoid small and medium businesses for anything that is not secured by property.

Unsecured business loans are also much harder to obtain through a traditional bank.

They are very heavy on documentation requirements in the application process and approvals can be slow.

Non-bank lenders are much more flexible and accommodating for both secured and unsecured loan types.

They prioritise speed and cash-flow underwriting and can approve low-doc applications in hours (sometimes minutes).

However, their credit policies differ significantly and knowing which is most suitable to your business is critical to a fast turnaround.

Our brokers can match you with the best lender for your business finance needs in minutes, so click below to get in touch.

Pros and Cons: Secured vs Unsecured Business Loans

To help you quickly weigh your options, here is a breakdown of the primary advantages and disadvantages of each loan type.

Secured Business Loans

Pros:

- Lower Interest Rates: Because the lender’s risk is reduced by the collateral, they can offer much sharper pricing.

- Higher Borrowing Limits: Loan amounts can easily scale into the millions if backed by high-value commercial equipment, vehicles, or property.

- Longer Repayment Terms: Terms can be stretched out to match the lifespan of the asset, keeping your monthly repayments lower and protecting daily cash flow.

- Accessible for Lower Credit Scores: If your financials aren’t perfect, having a strong physical asset to pledge can be the key to getting an approval.

Cons:

- Risk of Asset Loss: If you default, the lender can repossess the specific asset. Losing a critical vehicle or piece of equipment could immediately halt your business operations.

- Slower Settlement Times: Unless you are applying for a low-doc vehicle loan, the process can take longer due to required asset valuations, insurance checks, and PPSR registrations.

- Upfront Costs: You may need to cover the costs of bespoke valuations or legal fees to get the loan established.

Unsecured Business Loans

Pros:

- Fast Funding: The application process requires less paperwork regarding assets, allowing non-bank lenders to approve and settle funds in as little as a few hours.

- No Upfront Collateral Required: You don’t need to pledge a specific physical asset like a vehicle or property to get the funding.

- Highly Flexible: Perfect for bridging short-term cash flow gaps, paying unexpected invoices, or funding immediate growth opportunities.

Cons:

- Higher Costs: The increased risk to the lender means you will face higher interest rates and potentially higher establishment fees.

- Shorter Loan Terms: You are generally required to pay the funds back much faster, which can put a heavy burden on your ongoing cash flow.

- Lower Borrowing Caps: Maximum loan amounts are typically restricted (often capped between $500k and $1M) based strictly on your revenue and time in business.

- Still Carries Personal Risk: While not tied to a specific asset, lenders will almost always still require a Director’s Guarantee or a General Security Agreement (GSA).

Frequently Asked Questions

Is an unsecured business loan truly unsecured in Australia?

Rarely. Most lenders mitigate risk by requiring a personal guarantee or a General Security Agreement over your business.

Do I need a personal guarantee on a secured loan?

Almost always. Lenders demand a director guarantee alongside collateral to keep you personally liable if the business defaults.

Should I take unsecured business loan now and refinance later?

Fast unsecured cash can solve immediate capital needs. Once your financials strengthen, you can often refinance to a cheaper secured rate if you have an asset to use as collateral.

Which Business Loan is Right for You?

When comparing secured vs unsecured business loans, the right solution is largely dependent on what you plan on using the funds for, and how fast you need it.

If you need a vehicle, these are quick and easy to turnaround in a secured loan with a great rate attached.

Whereas a more complex asset that requires a bespoke valuation is going to take longer.

Unsecured loans are generally more expensive, but can be approved and funded the same day if the right boxes are ticked.

This is a great option for urgent, short-term needs where the cash flow is there to support the higher repayments.

Contact Gusto Finance to compare rates, terms, and security structures. We match you with the right lender and provide written confirmation of all guarantees before you sign.