While most riders opt for a straight up secured bike loan when getting new wheels, there are lease options available in the market.

This only suits very specific cases and your choice is usually a trade-off between cashflow, flexibility, and total cost.

In this article, we’ll compare motorcycle leases with regular bike finance so you can make an informed choice.

Key Takeaways: Lease or Finance a Motorbike

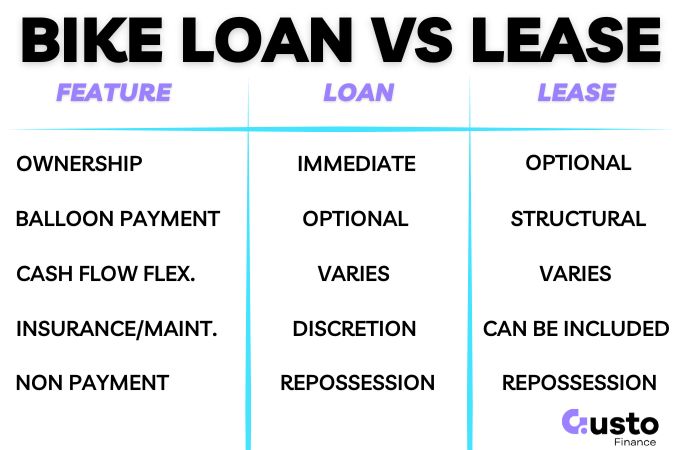

| Difference Between Buying and Leasing | When you buy (finance) a motorcycle, you own it and can modify it. When you lease, you are essentially renting it for a fixed term, with strict usage rules. |

| Why Lease a Bike? | Leasing allows for regular upgrades to new models, potential tax benefits for business owners, and lower repayments. |

| Lease Restrictions | Leases may come with mileage limits, fees for excess wear and tear, and financial penalties if you break the contract early. |

| Financing a Bike | Buying with a secured loan avoids mileage limits, can bundle your riding gear into the loan, and actually own the asset at the end of the term. |

Motorcycle Ownership Options

Leasing vs Buying a Motorcycle

When deciding between a lease or buying a motorcycle, most people focus on the monthly payment.

Instead, you should base your decision on practical variables that affect you.

These can include:

- How long you plan to own or use the motorbike.

- Your intended use, and if its for business purposes.

- Maintenance costs and responsibilities.

- The amount of riding you will do annually.

- Repayments and cashflow requirements.

As a general rule, leasing tends to suit people wanting regular upgrades, and those seeking a predictable short-term commitment.

For business owners, a lease comes with a range of tax deductions that could be advantageous in some circumstances.

Whereas buying is more suitable to those planning to use a bike long term and those wanting to modify their bikes.

Finance for a Motorbike

Buying your motorcycle gives you the freedom to ride the bike as much as you like without penalty, and make modifications without restriction.

You can also sell it whenever you like with your only risk being an early repayment fee on your motorbike loan (if applicable).

A secured motorcycle loan will get you the best interest rate on your finance, and you could also factor in a balloon payment to keep your repayments low.

However, you will be responsible for all maintenance costs, insurance, and everything else associated with running the bike.

Given that you own the asset you will also have to wear any depreciation over time as an additional cost of ownership.

Get a quote on your motorbike finance options below. Our team have access to over 50 lenders and can find you the best deal for your circumstances.

Leasing a Bike

There are two common lease structures to consider for your motorbike:

- Finance lease: You pay for the bike’s use plus a finance charge, with a residual value set at the end. Maintenance is often not included.

- Operating lease: This acts like a managed rental. It may include routine servicing, but only if explicitly stated.

Lease repayments can look lower because you avoid paying the full purchase price during the term.

Instead, a large lump sum known as a residual or balloon payment remains at the end.

When the contract finishes, you must return the bike, refinance the balance, or pay the residual to keep it.

So you often have the option to retain the bike if you want to take ownership.

This structure introduces a residual shortfall risk. If the motorcycle’s market value drops below the final payout figure, you may need to cover the financial gap yourself.

This risk is contract dependent, so always confirm your specific terms and maintenance inclusions in writing.

When leasing a bike you should also be very clear on the inclusions in the contract.

Things like insurance, servicing, and general maintenance all impact your total cost of ownership and being clear on this prior to signing an agreement will limit future surprises.

Motorcycle Contract Conditions

Your contract will include a number of obligations for you, and conditions that must be upheld to avoid additional fees.

The most common considerations in a lease or finance contract are below.

Insurance requirements

Whether you are leasing or financing your new bike you are going to be required to have comprehensive insurance with the lessor, or lender, listed as an interested party.

This is to ensure their interests are covered in the event of an accident.

However, an insured amount may not cover your full liability under the contract. So you should be weary of this, particularly early on in the agreement.

Early termination penalties

Leases can be very expensive to break and should not be treated as a try-before-you-buy option.

A bike loan may also have an early payout fee up to a certain point, but this is likely to be much cheaper.

You should understand both possibilities before selecting your finance of choice.

Mileage and wear charges

Lease contracts can enforce strict per-kilometre excess fees.

Expect excess wear disputes when returning the vehicle, as tyres and brakes are treated as your consumables.

Whereas with a bike loan there are no such restrictions.

Gear bundling

New riders need a helmet, jacket, gloves, and security.

Some finance structures allow bundling these upfront costs into your loan, provided it fits the lender’s policy.

Compare Lease or Buy Motorcycle Costs

It can be difficult to compare costs accurately due to the difference in outcomes, and inclusions between a lease and finance contract.

However, if cost is your primary decision factor then follow the steps below to reach an approximate comparison point.

- Document the on-the-road price or lease start value and your term length (e.g., 36 months).

- Get insurance quotes for the required level of coverage.

- Add total monthly payments to all establishment, administration, and account fees.

- Add maintenance assumptions. Only count servicing as included if explicitly written into your contract.

- Calculate your exit scenario (if any).

- Subtract the expected resale or trade-in value at three years.

This will give you some idea of the total cost of ownership.

If the monthly payment is more important to you then you can skip all this and just look at the payments nominated in your agreement.

Frequently Asked Questions

Is motorcycle lease maintenance actually included?

Maintenance is only included if you select a full-service operating lease. Standard finance agreements leave you responsible for all mechanical servicing. You must carefully check your contract terms to confirm if costly consumables like tyres and brake pads are covered before signing.

Can I get out of a motorcycle lease early?

You can terminate early, but it is often very expensive. Lenders will calculate a final payout figure based on your remaining term and residual value. Ask your provider for their exact termination formula upfront.

Is it smarter to lease or buy a motorcycle if I am a new rider?

Deciding to lease or buy a motorcycle as a beginner depends on your riding plans. Leasing works if you keep your kilometres low and accept strict modification restrictions. However, buying a used, learner-friendly bike with a smaller secured loan is usually smarter to avoid expensive lease return penalties.

To Lease or Buy Your New Motorcycle

Leasing delivers lower monthly payments and regular upgrades. However, you must carefully manage:

- Residual value risks

- Strict insurance rules

- Kilometre limits

- Expensive early exit costs

Whereas buying secures total ownership and freedom from day one.

This is a better choice for most people, unless there is a tax advantaged reason to go for the lease.

If you’re in the market for a new bike get in touch with the team at Gusto Finance to instantly access a panel of 50+ lenders so you can get the best rates.