You can still get motorcycle finance if you have had credit problems in the past but it is likely to be at a much higher interest rate.

A bank is not going to touch you, but there are specialised lenders who will assess you on your current financial behaviours and not just your credit history.

In this article, we’ll discuss how to secure motorbike finance with bad credit and how to improve your chances of approval.

Key Takeaways: Bad Credit Motorbike Finance

| Can I Get Approved with Poor Credit? | Yes, specialist non-bank lenders offer second-chance bike finance if you meet their criteria. |

| Expected Bad Credit Terms | You will face higher interest rates and fees. Borrowing limits are lower, and the motorcycle must be viable security. |

| Approval Levers | Stable income, clean recent banking conduct, a cash deposit, and a sensible bike choice are all positives. |

| High Risk Indicators | Recent arrears, payment reversals, or frequent BNPL and wage advance usage will lower your chances of approval. |

What Lenders Consider Bad Credit

Your credit score is a measure that is based on your credit history. This is used to determine the likelihood of a future default event.

The lower the score, the greater the likelihood that a loan will not be repaid.

As a result, it will be more difficult to get a loan for a new bike and the cost of that loan will be higher.

High risk indicators include:

- A low credit score

- Unpaid defaults or recent arrears

- A Part IX debt agreement or bankruptcy

- A thin credit file

However, past mistakes are rarely deal-breakers if you have built up a track record of reliable income and clean banking since.

What Lenders Review Beyond Your Credit Score

Specialist lenders look beyond the just credit report and a number of five key areas to develop a better rounded view of your risk profile.

This is a positive for those who have made the effort to recover after a financial setback, and makes it easier to get a motorcycle loan approved.

Credit File

Recency and severity matter of adverse events matter most.

A three-year-old default that has been paid off long ago may hurt your chances far less than a missed payment last month.

Serviceability

Lenders require stable employment and a consistent cash surplus after your living expenses to prove that you can afford the repayments.

A track record of savings is also helpful.

Banking Conduct

Clean bank statements are non-negotiable.

Lenders reject applications showing overdrawn accounts, repeated fees, or direct debit reversals.

Other high-risk transactions to avoid include frequent gambling and use of wage advance services.

Application Behaviour

Each application results in a hard credit check and is visible to the next lender

Submitting multiple applications in a short space of time can further damage your credit score and lead to rejection.

While it is wise to shop around for the best deal, it is much safer to do this through a broker who will do a soft credit check upfront, which is not visible to other lenders.

A formal application will only be done once you are matched with a lender who is likely to approve the loan.

Click below to get in touch with the Gusto team and start the process.

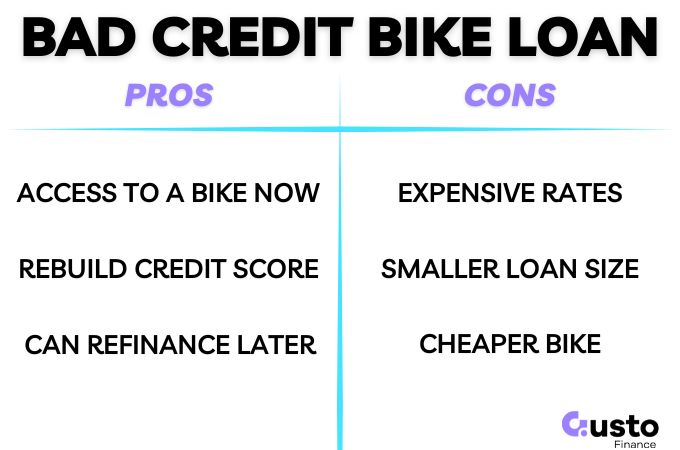

The Cost of Bad Credit Motorcycle Finance

Lenders use risk-based pricing for bad credit loans. Your credit history directly dictates your final loan structure:

- Interest rates: Expect a wide band between 14% and 29%.

- Fees: Check your loan schedule for larger establishment fees, risk charges, and early payout penalties.

- Borrowing limits: Poorer credit restricts your maximum loan size and requires a higher cash deposit.

- Loan terms: Your repayment timeline is capped by your budget and the bike’s age at the contract end.

The worse your credit history the tighter the loan conditions and higher the fees and interest will be.

6 Steps to Improve Your Motorcycle Finance Chances

Follow this checklist to position your application to overcome any negatives in your credit history.

Step 1: Clear Any Arrears

You will not be approved for a bike loan if you are behind on any current loans you have elsewhere.

Until everything is up to date you should not be taking on extra credit anyway.

So get things paid up and re-assess your position from there.

Step 2: Bank Statement Hygiene

Make sure your bank statements are showing reliable patterns of income, repayments, and no high risk transactions.

A bad credit lender will look at 90 days of transactions and you should look to avoid payment reversals, income fluctuations, and high risk transactions throughout this period.

Doing so may also help you develop some positive financial habits longer term also.

Step 3: Minimise Buy Now Pay Later Use

Reduce Buy Now Pay Later usage to simplify your liabilities.

BNPL is a short term liability that can be calculated as a long term limitation in your budget.

So lower credit limits, or close down accounts prior to applying so that your current debt is as low as possible.

Step 4: Save a deposit

The best way to demonstrate good financial management is to have a consistent savings track record.

When taking on a new loan it helps to demonstrate that you are saving that much every month now and that the additional commitment can be met comfortably.

A big positive when overcoming a low credit score.

Step 5: Use a broker

Get a pre-assessment to find the right lender without risking hard credit enquiries damaging your credit file further.

How Bike Choice Impacts Your Approval

Securing motorcycle finance with bad credit is easier when you choose a common, sensibly priced model rather than a niche performance bike.

Being on a learner licence does not automatically exclude you.

However, lenders will factor expensive LAMS insurance premiums into your affordability assessment.

Where possible you should buy from a dealership so you have warranty and other consumer protections.

Private sales are possible, but require extra administrative work, including mandatory PPSR checks, strict seller verification, and condition reports.

You may also cop some extra fees from a lender when its a private sale to cover the cost of processing the above information.

Frequently Asked Questions

Can I get motorcycle finance with defaults or a bankruptcy?

Yes, but approval is assessed on a case-by-case basis. Specialist lenders will consider applicants with discharged bankruptcies or defaults. You must expect higher interest rates and stricter lending conditions.

Will a Learner licence stop me getting finance?

Not necessarily. Lenders care more about your stable income and overall affordability than your licence tier. The real hurdle is the cost of insurance, which is mandatory for a secured bike loan.

What documents will I typically need for a bad credit bike loan?

You must provide a valid photo ID and recent proof of income. For credit-impaired files, lenders also require three months of clean bank statements to verify your living expenses and confirm a regular cash surplus.

Can I use a guarantor for a motorbike loan if I have bad credit?

In theory, adding a guarantor can improve your chances of approval or help secure a better interest rate. However, lenders rarely accept guarantor loans. A co-borrower is a more viable option but both borrowers need to show they get genuine benefit from the bike.

Bike Loan Next Steps

Successful approval of a motorbike loan with poor credit comes down to three key factors:

- Matching your application with the right lender policy.

- Showing clean recent banking conduct.

- Proving you can afford the total cost of repayments, insurance, and gear.

Protect your credit score and avoid multiple rejections by running a pre-check before submitting any formal applications.

Gusto Finance offers fast, online assessments to match you with a specialist lender.

Request a free quote below to review your options and get on the road.