When financing a second hand motorcycle it is critical that you get the best deal on finance, while also making sure you are buying a good quality bike.

It is tempting to seek out a bargain from a private seller. But this comes with risk, extra work, and could mean a more expensive loan.

Whereas a dealership may offer a quick, easy, and safer option.

The higher purchase price could also be offset by lower finance costs, if you know where to look.

In this article, we will discuss the financial aspects of financing a 2nd hand bike while also covering how to minimise the risk of buying something dodgy.

Key Takeaways: 2nd Hand Bike Finance

| Secured vs. Unsecured | Newer used bikes can qualify for a Secured Loan which are generally cheaper. An older or lower value bike may require an Unsecured Loan. |

| Insurance Mandate | A secured loan will require Comprehensive Insurance which comes at a cost. CTP alone will not satisfy their requirements. |

| Dealership vs. Private Sale | 2nd hand dealership sales are easier to finance and come with consumer protections. Private sales require more work and carry additional risk. |

| PPSR Checks | If buying privately, you must do a PPSR check. This ensures the seller doesn’t have an outstanding loan on the bike, or was a past write off. |

Define Your Motorcycle Budget

To secure loan approval for a second hand motorcycle, you must prove you can manage the total cost of ownership without facing financial hardship.

Define your budget properly by factoring in these mandatory on-road and ownership costs before applying:

- Registration and comprehensive insurance.

- Regular servicing and consumables (tyres, chains, brake pads).

- High-quality protective gear.

You may be able to roll in some of these costs to your loan if you can afford the repayments.

Alternatively, you can tip in some cash as a deposit on the purchase if you want to keep your loan size a bit lower.

While not always required, paying a deposit upfront lowers the total interest charged over the life of the loan.

If you are not sure what repayments you can afford, click below for a free consultation with our expert brokers.

They can do the sums for you so you know how much you have to spend.

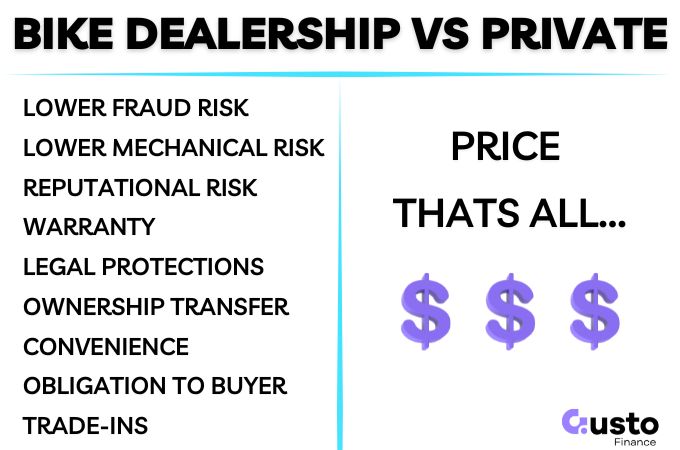

Buy Privately vs a Dealership

On balance, you will be much better off financing a second hand motorbike from a dealership than a private seller.

Yes, you may be able to land a great deal privately, but you will be losing a number of important protections by doing so.

Dealership Sales

A dealership has a number of obligations that de-risk the transaction for the buyer, and also the lender financing the bike.

As a result, financing can work out cheaper when buying through a licensed dealer.

These obligations and guarantees can include:

- Statutory warranties.

- Roadworthy certificates.

- Compulsory vehicle history declarations (such as being a repaired write off).

- PPSR checks (no finance owing on the bike).

- General consumer protection law.

- Dealership reputation.

In addition to all of this, the paperwork and coordinating settlement with the lender funding the purchase will be much less work for the buyer.

Private Sale Motorcycle Finance

If you are willing to do the legwork you can certainly finance a second hand motorcycle.

Just expect the process to take longer and you’ll have to do a bit more work.

Lenders also view private sales as a higher fraud risk. To protect all parties, they require strict asset verification.

You must provide:

- Clear photos of the bike

- The Vehicle Identification Number (VIN)

- Current odometer readings

- Concrete proof of ownership

To further control risk, lenders release the loan funds directly to the seller rather than paying you.

Discovering the seller still owes money on the bike is a common source of problems in private sales.

The previous lender can legally repossess your new motorcycle if that finance is not cleared as part of the purchase.

Your new lender will either pay out the existing loan directly to clear the encumbrance, or require the seller to clear the debt before the transfer.

Because these security checks take time, and can require personal information to be handed over, private sellers often lose patience.

Which leaves you back at square one.

PPSR and VIN Checks for Used Bikes

As part of your asset verification you’ll need to check the Personal Property Securities Register (PPSR).

By obtaining a PPSR certificate you can be sure if the bike has an existing encumbrance, meaning money is still owed to another lender.

It also flags if the motorcycle is recorded as stolen or a repairable write-off.

Lender Requirements for a 2nd Hand Bike Loan

The financial side is the same as any other loan product, with the only variation being if it is a consumer or commercial loan (bike being used for business purposes).

Your credit history and finances will be assessed to determine your capacity to repay the loan, and what interest rate is appropriate for your risk profile.

Your loan term is also a big factor in determining the required repayments and the total cost of the loan.

A typical bike loan term is 36 to 60 months, but can go up to 84 months in some circumstances.

However, the longer the term, the higher the interest costs over time.

Quality of Security

You will get the best deal on finance if you are using the motorcycle being purchased as security for the loan.

However, secured lenders will require an active comprehensive policy before authorising settlement.

Compulsory Third Party (CTP) insurance does not meet this condition because it only covers personal injury, whereas comprehensive policies protect the lender’s physical collateral.

This is an extra cost you’ll have to factor in.

A second hand bike will also need to meet the lender’s criteria for eligible collateral for this to be possible.

This could be difficult if you are buying a much older bike, and is just as important as meeting the financial criteria for your loan approval.

However, if the motorbike doesn’t qualify as security you still have options.

Unsecured Bike Loan Options

If your target motorbike is not eligible as security with any lender, then you can opt for an unsecured loan.

This requires no security and offers maximum flexibility. But the interest rate is likely to be higher.

There are some benefits to consider in addition to the higher cost.

You can sell the bike without having to involve the lender, as there is no security registered on the PPSR.

So you are free to do with the asset as you please.

If you were to fall behind on your loan repayments then the lender also cannot easily repossess the bike.

It could still happen after a judgement and court order is obtained, but its not as easy as with a secured loan.

Secured vs Unsecured Motorcycle Loan Summary

Given the value of a second hand bike can vary significantly there are pros and cons of both loan types.

As a quick summary of all that has been discussed so far, a secured or unsecured loan would be most suitable in the following circumstances.

Choose a secured bike loan if:

- You want the lowest possible interest rate.

- The bike is eligible for security.

- Mandatory insurance is ok.

- You plan on owning long term

- The value of the bike is above minimum loan sizes.

Choose an unsecured bike loan if:

- You are buying a bike under $5,000.

- The motorcycle is a vintage or older model.

- You don’t want to insure the bike.

- You want to skip the vehicle verification process.

- You may want to sell quickly in the future.

Why Use a Broker For a Second Hand Bike Loan?

Applying directly to multiple lenders will damage your credit score and delay your purchase.

An expert broker can avoid unnecessary applications by pre-qualifying you for the most suitable lender.

We match your financial profile directly to a lender whose policies align with your credit profile, while offering the best deal possible.

This eliminates the guesswork and gets your motorcycle loan settled faster, while also ensuring you have the lower rate possible.

Frequently Asked Questions

Can I finance a used motorcycle from a private seller?

Yes, you can secure a loan for a private purchase, but expect stricter lender requirements. Lenders will run PPSR checks, verify the VIN, and pay the seller directly to prevent fraud. This process takes slightly longer than a dealership purchase.

Is it better to use a personal loan for a cheap used bike?

Yes, an unsecured personal loan is usually the most practical option for motorcycles priced under $5,000. While unsecured loans carry higher interest rates due to a lack of collateral, they offer maximum flexibility and allow you to skip strict vehicle age requirements entirely.

Do I need a deposit to finance a second-hand motorcycle?

A deposit is rarely required to secure an approval. However, contributing upfront cash reduces your total loan amount and lowers your ongoing interest costs. It can also improve your chances of approval if you have a lower credit score by reducing the lender’s overall risk.

Securing Used Motorcycle Finance

There are plenty of lenders who will fund a loan for a second hand motorcycle, both private and dealership sales.

However, the process required to get to settlement and the quality of outcomes can vary significantly based on the bike and your credit history.

If you don’t know where to start, and would benefit from a helping hand establishing your budget and likely costs involved then click below to get in touch with Gusto Finance.