Car loans are long-term financial commitments and it is common for a borrower’s circumstances to change over the repayment period.

If the change is positive then cheaper and better car finance options can become available. And if you are a good customer then a lender (but not all) may bend over backwards to keep you!

What if the change is negative? Will your lender accommodate longer repayment periods?

These are all scenarios where refinancing your car loan with the same lender would be considered.

In this article, we’ll discuss how to determine if this is the right choice for you or if you should look elsewhere to get the best car loan possible.

Key Takeaways: Refinance with Same Lender

| Is it possible? | Yes, most lenders allow you to refinance internally (often called a “loan variation” or “restructure”) if you meet their current credit criteria. |

| Why do it? | The main reasons are to lower monthly repayments by extending the loan term, remove a guarantor/co-signer, or pay out a balloon payment. |

| The Loyalty Myth | Don’t assume your current lender will give you the best rate. They often reserve their best deals for new customers, so shopping around is critical. |

| Fees to Consider | Even with the same lender, you may still face early repayment fees on the old loan and establishment fees on the new one. |

| Credit Assessment Risk | Applying for an internal refinance triggers a new credit check. If your credit score has dropped, they could decline you. |

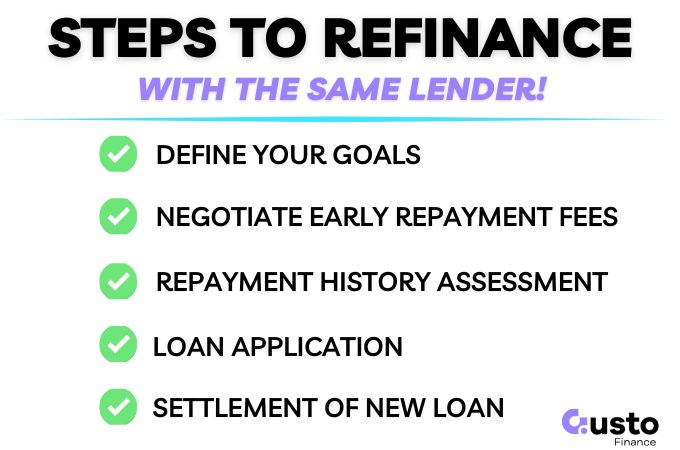

Internal vs External Refinancing

Car loan refinancing is when you replace your existing loan with a new one.

A loan is usually refinanced if there are better terms available to the borrower compared to their current loan.

For example, a lower interest rate and a reduced monthly repayment.

Auto finance is a competitive market and new deals may be accessible by the borrower at any time.

As a result, most refinances are to a different lender so that a borrower can take advantage of better deals elsewhere.

This is an external refinance and is much more common than refinancing with the same lender (and internal refinance).

If you would like to explore your options in the market today then submit an inquiry below and our brokers will be in touch.

Will My Current Lender Approve a Refinance

You can usually refinance a car loan with the same lender if you meet all of the required criteria.

Lenders make money from interest and fees, so keeping you as a customer long-term is usually beneficial to them.

However, some lenders don’t actively promote refinancing because it means renegotiating terms that might reduce their earnings.

Other lenders will not offer refinancing at all.

If they do, then you are still going to have to meet their lending criteria on the day of your new refinance application.

4 Criteria Lenders Check Before Approving You

1. Repayment History

The lender now has access to your repayment history of the current loan and will take this into account when assessing your refinance application.

If you have not made all of your payments on time this could hurt your chances of being approved.

Whereas an alternative lender may not see this if you correct the problem quickly.

2. Age of the Loan

A refinance will only make sense for the lender if you have repaid a reasonable amount of the principal first.

In the first 12-18 months of your car loan, the balance may be higher than the value of the car so adding any administrative fees from the restructure could lead to a higher loan-to-value ratio than a lender will allow.

The lower the loan balance the more flexibility you are likely to have with your lender as their risk of extending further credit, or the repayment period, is lower.

3. Age and Value of the Car

Lenders also have vehicle-specific criteria for what they will and will not lend against.

If a couple of years have passed then your car may have exceeded a threshold such as age, or kilometers on the odometer.

You may still be able to refinance with the same lender but you may only qualify for an inferior product that would make you worse off.

4. Standard Credit Assessment

When creating a new loan with different terms a lender will be obligated to conduct a complete credit assessment.

If your financial situation and credit score have improved then no problem.

But, if things have deteriorated then you may not be approved.

Benefits of Staying With Your Current Lender

Extending the Loan Term to Lower Repayments

If you have had a change in your financial circumstances and would like to free up cash flow then you could refinance to extend the term of your loan.

Let’s say you have two years of repayments remaining, if the value and age of your car are acceptable, then you could extend that payment term to five years.

This would have a significant impact on your repayment amount but will cost you much more over the extended loan term.

For example, if you have $15,000 left to pay on a loan with two years remaining at 10% interest then your monthly repayment is $692.17.

If you were to refinance to extend the loan term to five years your payment would come down to $318.71.

While the lower repayments sound great, it would cost you an additional $2,510.17.

Removing a Co-Signer or Guarantor

If you needed a co-signer or guarantor to get approved for the loan in the first place, but your financial situation has improved, refinancing can allow you to remove them from the agreement.

This can give you additional freedoms while also freeing up the co-signer from any obligations that could inhibit their ability to get credit elsewhere.

Car loans are typically repaid over 4-7 years. This is a long time for a third party to be tied to the finance and is a common reason to refinance with the same lender.

Removing a Balloon Payment

Some car loans come with a balloon payment, which is a large lump sum due at the end of the loan term.

If you do not have access to the lump sum at the time it is due then refinancing can allow you to pay this over time.

This is another example where the overall cost will be much more significant but unless you have savings or are selling the car it may be unavoidable.

Potentially Avoid Early Repayment Fees

One of the biggest obstacles to refinancing a car loan is the break fees that most lenders will charge to close your loan early.

The benefits of a refinance must outweigh the cost of these fees.

However, if you are refinancing with the same lender you may be able to negotiate this fee as you will continue to be a customer.

Perhaps a more moderate administrative fee would be achievable, or perhaps no fee at all. Any extension in a repayment term will earn the lender more money anyway so it is worth asking the question.

What If Your Lender Says No?

If your lender either won’t allow refinancing, or their product offering isn’t competitive, get in touch with Gusto Finance today.

We have access to over 40 lenders are can find the most suitable option to meet your refinance objectives.

You may be able to save thousands if you refinance with the right lender so it always pays to shop around.

Should You Stay or Switch?

Refinancing a car loan with the same lender can make sense in the right circumstances.

You may find your current lender is keen to retain you as a customer and could offer a favourable refinance option.

If the long-term cost is acceptable then this can be a great option.

However, it is always worthwhile looking around at what options are available in the market so you know you are getting the best deal.