While using services like Afterpay or Zip may not solely lead to your car loan being declined, it can have a negative impact on your capacity to repay your loan.

Overuse of these services can also be a warning sign to lenders that you may not be managing your household budget well.

Things like high credit limits, stacked repayments, missed payments, and recent enquiries can all compound to place you in a higher risk category.

In this article, we’ll discuss how lenders may interpret your use of BNPL and the ways it affects your car loan application.

Key Takeaways: BNPL

| Credit Report Visibility | Due to recent credit regulations, creating a new Buy Now, Pay Later accounts triggers a formal credit check. Lenders can see this on your credit file. |

| Balance vs Credit Limit | Some lenders calculate your borrowing power based on your maximum approved BNPL limit, not your current balance. |

| BNPL Stacking | Using multiple BNPL apps at the same time signals financial stress to lenders. It shows a reliance on future income to fund short-term, everyday expenses. |

| Bank Statement Red Flags | If a lender asks for bank statements, they will look for missed BNPL payments, late fees, or using BNPL for essential daily living expenses. |

How Lenders Actually See Your BNPL Accounts

In the past, Buy Now, Pay Later (BNPL) debts were invisible to auto lenders unless they looked at your bank statements.

Which is usually not required.

However, due to recent credit regulation reform all new BNPL applications require a credit check.

This leaves a mark on your credit file and a clear record of enquiries.

Low Cost Credit Regulations

From June 2025, BNPL providers have been required to conduct a responsible lending assessment.

Opening a new account or increasing your limit will trigger a formal credit check.

This legislation gives auto lenders more consistent visibility into your spending without the blind spots that could previously only be filled by scrutinising bank statements.

This does not mean BNPL users will automatically get rejected for car finance.

It simply means your payment behaviour and total debt exposure are officially recorded and easier to verify.

This works in favour of those with good spending discipline, and protects those overspending from taking on additional debt they cannot afford.

However, there are still visibility limitations that can leave BNPL users disadvantaged through the eyes of a conservative lender.

How Lenders Calculate BNPL in Your Borrowing Power

Lenders are required to assess your serviceability to ensure your income comfortably covers all commitments before approving any loan.

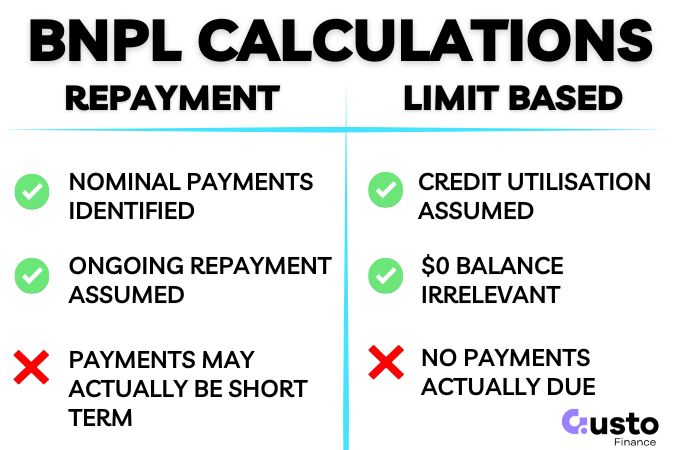

When evaluating Buy Now Pay Later (BNPL) accounts, they use one of two methods.

Repayment-based

Lenders count the actual recurring BNPL deductions visible on your bank statements.

The assumption is often made that this liability is ongoing, even if you only have one or two payments left outstanding.

This can unfairly penalise the borrower if it is a one off purchase.

From the lender’s point of view it is as likely that you will continue to use the BNPL account and the repayments will be ongoing.

Limit-based

Some lenders treat the BNPL facility like a credit card.

They apply a notional monthly repayment of around 3% against your maximum available limit, regardless of your current balance.

This explains why paying your balance to $0 sometimes fails to improve your repayment capacity.

Under a limit-based assessment, an open account still reduces your borrowing power because lenders assume you could max out the approved limit tomorrow.

To instantly boost your car finance approval chances, close unused accounts and reduce excess limits before applying.

Stacking BNPL Plans

Why does $500 spread across five payment apps look worse to a lender than a $5,000 personal loan? Predictability.

Stacking three to five BNPL plans creates chaotic repayment dates scattered across your month.

Lenders prefer one structured debt over many micro-debts because a single schedule reduces the chance of payment surprises.

Juggling multiple providers signals a tight cash buffer and heavy reliance on future income to fund short-term spending.

Less buffer equals higher perceived risk, which lowers your approval odds or triggers stricter loan conditions.

BNPL Bank Statements Red Flags

A lender will only require bank statements in circumstances where they need to look closely at your financials.

For example, if you have past defaults on your credit report or a generally low credit score.

In these cases, they will look at 90 days worth of bank statements where the following red flags could harm your application:

- Stacking multiple active BNPL accounts simultaneously.

- Scheduling repayments every week with no gap between plans.

- Incurring late fees or missed payments of any size.

- Relying on BNPL for everyday essentials like groceries or fuel.

- Operating with low end-of-month balances or frequent overdrafts.

The good news is that even if you have some of these issues embedded in your recent bank statements, you can fix this in just a few months.

90 Day Bank Statement Cleanup

You can improve your car finance approval odds by following this timeline before submitting an application.

- List every BNPL account, limit, and repayment frequency using your last 90 days of bank statements.

- Pay down active plans and stop opening new ones.

- Close unused BNPL facilities or reduce limits. Keep all closure confirmations.

- Keep bank statements consistent and predictable.

When you do apply for your loan you may be asked about your BNPL usage if it appears on your credit file.

By confirming that your accounts have been closed it will negate much of the negative impact of the previous usage in regards to your repayment capacity.

Frequently Asked Questions

Will BNPL automatically get my car loan declined?

No, using a Buy Now Pay Later service will not automatically result in a declined car loan. Lenders assess your overall affordability and look for risky spending patterns rather than rejecting you just for having an account.

Is it better to pay off BNPL or close it entirely before applying for a car loan?

Closing the account is the safest option before applying for vehicle finance. Paying off your balance helps cash flow, but many lenders still treat your maximum available limit as an active monthly commitment. Closing the facility removes this debt calculation completely.

Will a BNPL sign-up hurt my credit score?

Under new responsible lending laws, opening an account or requesting a limit increase will leave a formal enquiry on your credit file. This application footprint is highly visible to auto lenders, and multiple recent enquiries can temporarily lower your score.

What if I am declined for a car loan due to BNPL?

A rejection does not mean you are entirely out of options. Every auto lender assesses risk differently. If a bank declines your application, a specialist broker can step in. We can help you close accounts, restructure your application, and match you with a flexible lender that suits your current profile.

Manage BNPL Usage Prior to Car Loan Application

Lenders treat Buy Now, Pay Later products as active debt. To maximise your car loan approval odds, remember these three rules:

- Visibility is now high due to mandatory credit checks.

- Limits shrink borrowing power even if the balance is $0.

- Improve your bank statements in less than 90 days.

Unsure how lenders will assess your transaction history? Get in touch below.

The brokers at Gusto Finance can sanity-check your statements and match you to a lender policy that fits your profile.