ABN holders have access to a range of commercial finance products that can fund a new vehicle or equipment for your business.

They are flexible, accessible, and often can be secured with minimal paperwork.

For those with bad credit, you may have a few more hoops to jump through but approval is still achievable.

Bad credit usually means higher interest rates and stricter lender conditions.

In this article, we will discuss what options are available to self employed business owners who need finance but have had credit issues in the past.

Key Takeaways: Bad Credit Business Loans

| Will Credit Issues Exclude me from Business Car Finance? | While an adverse credit event may limit your choice of lender, there are options that specialise in bad credit finance. |

| Low-Doc Flexibility | ABN holders may have access to Low Doc loans that require less paperwork and faster approvals. |

| Expect Higher Interest | A commercial car loan might be ~6% to 8%, but with bad credit it could be 12%–20%+ range depending on the credit issues. |

| Property Owner | This is a major green flag for lenders. It can open doors to Low Doc approvals even if your credit score is low. |

| Large Deposit | A larger deposit (10–20%) lowers the lender’s risk (LVR) and can assist secure an approval with bad credit. |

Understanding Vehicle Finance for Business

Business vehicle finance is a loan or lease used to buy a vehicle that is used predominantly for business purposes.

The car, ute, or van you purchase acts as security for the finance.

Because the loan is secured against a tangible asset, it lowers the lender’s risk.

This creates more pathways to an approval, especially for those with a lower credit score.

Basic eligibility requires an active ABN, usually with at least 6 months trading history, and ideally being registered for GST.

A low-doc loan is the fastest and easiest way to secure finance. But if you have a low credit score it will be more difficult to qualify for this type of product.

Eligible Credit Scores for Business Finance

Your credit score provides a useful snapshot of your financial history, but lenders consider many factors beyond this.

Bureaus like Equifax, Experian, and Illion use different scales, but the specific listings on your file matter most.

As a general guide, the following ranges can be useful so you know where you stand as a regular consumer (Equifax CCR Score).

- Very Bad Credit – <200

- Bad credit – 200 to 400

- Fair credit – 400 to 600

- Good – 600 to 800

- Very good – 800+

When seeking commercial finance you really need a score >500 to access the easier pathway to approval via a low-doc loan.

While there are options below this, it will require more time and effort on your part to get approved.

Lenders will be most concerned with serious adverse listings like defaults, court judgments, or past bankruptcies.

Lenders also consider your recent conduct; a history of stable income and clean bank statements can outweigh old credit issues.

So if you have a score <500 then you will need to make sure these additional documents are squeaky clean!

Setting Realistic Interest Rate Expectations

If you have bad credit you are not going to have access to the best interest rates on the market.

Lenders use risk-based pricing, so your final rate depends on their full assessment of your application.

Several factors can help lower your quote:

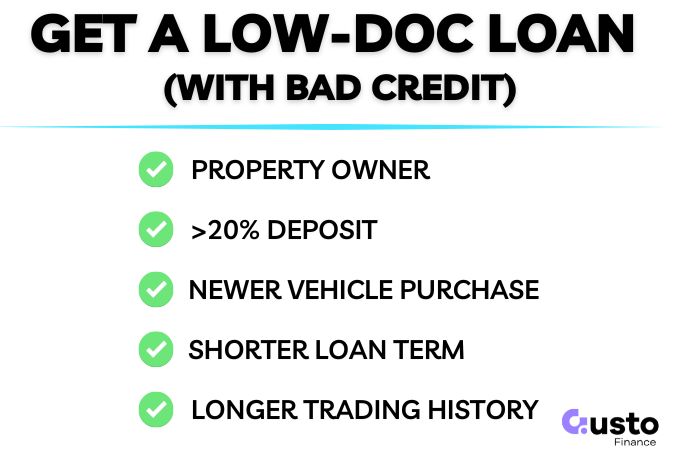

- Whether you are a property owner or not

- A larger deposit (lower Loan-to-Value Ratio)

- A newer vehicle (stronger security)

- A shorter loan term

- Strong business trading history

For the same $40,000 ute, an applicant with a clean file might secure an 6%-8% rate. An applicant with impaired credit could be quoted 14% plus a risk or establishment fee.

In extreme cases, the rate could even be higher than 20%.

Matching Your Application to the Right Lender

Applying to the wrong lender can lead to rejection and further damage done to your finance prospects.

The more problems in your credit report, the fewer options you will have. But how do you know which lender is best?

The answer is to apply through a broker who understands commercial auto finance, and has access to a broad panel of lenders.

This allows them to match your situation with the lenders who may accommodate your exact circumstances, and then selecting the most suitable loan product for you.

There are multiple tiers of lenders that may lend to you, and a broker will be able to look at the credit policies of each one BEFORE submitting a formal application:

- Major Banks: Offer the best rates but have the tightest credit policies. They are the least likely to approve applications with recent adverse listings.

- Non-Bank Lenders: This is where most ABN holders find success. They have broader policies, faster decisions, and more flexible criteria for minor credit issues.

- Specialist Lenders: Focus on second chance finance, assessing paid defaults or post-bankruptcy scenarios on their individual merits.

This strategic approach prevents multiple hard credit enquiries from damaging your file and gives you the strongest possible chance of approval.

Low-Doc and No-Doc Loan Requirements

While you might see ads for no-doc loans, the reality for ABN holders is low-doc, meaning reduced paperwork, not zero.

There are only a couple of things that are required for every low-doc car loan.

Without exception, you will be required to provide:

- Proof of ID; and,

- ABN Registration

GST registration can also be helpful as it generally shows that turnover is above the threshold required.

If you own property you can often fast track your way to an approval, even if your credit score is on the lower side.

When Additional Documentation is Required (Full Doc)

If you do not own property, and have an impaired credit history, a lender may request stronger evidence of your current trading health.

Be prepared to provide:

- 3–6 months of recent business bank statements

- Business Activity Statements (BAS), if GST registered

- An accountant’s letter

- Tax returns

Clean, consistent bank statements demonstrating your ability to manage repayments are crucial.

For a complete rundown of what to expect, see our guide on the low-doc application process.

Strengthen Your Application with These Key Levers

You can’t rewrite credit history overnight, but you can reduce a lender’s risk on the new loan.

Lower risk is often rewarded with better terms and a higher chance of approval.

Focus on these high-impact actions before you apply:

- Provide a larger deposit: This lowers the loan-to-value ratio (LVR), reducing risk and making your application attractive to more lenders.

- Choose a newer vehicle: A newer car with a strong resale value provides better security for the lender.

- Shorten the loan term: If your cash flow allows, this reduces the lender’s total risk exposure over time.

- Consider a guarantor: A guarantor with a strong credit profile can significantly strengthen your application.

To avoid damaging your credit file with multiple enquiries, always start with an eligibility assessment through a broker.

How to Handle Defaults and Past Bankruptcies

While a default or bankruptcy is a serious blemish, some lenders will focus more on evidence that the issue is resolved and firmly in the past.

There is no universal waiting period.

Some may consider you as soon as the default is repaid, others need at least 12 months, and some may exclude you for the full 5 year period it appears on your credit file.

You can strengthen your case with proof of stability, like consistent income and a stable address, plus a short, honest written explanation of what happened.

This is important context that a broker ill provide as part of your loan application, and will often speak directly to the lender to explain special circumstances.

FAQs

Can I get approved for a business car loan with a low credit score?

Yes, you can be approved for a business car loan if you apply to a lender that considers a low credit score and you meet their other criteria. A low-doc loan could still be possible if your trading history is strong. However, additional scrutiny may be warranted which will detailed business cash flow and bank statements.

Do lenders check my personal credit file, my business credit file, or both?

Most lenders assess both, particularly for sole traders and small businesses. Your personal credit conduct is seen as a strong indicator of your reliability and repayment capacity.

Will applying for a business car loan hurt my credit score?

A formal application results in a hard enquiry on your credit file, which can cause a temporary drop in your score. Multiple hard enquiries in a short period can signal financial stress to lenders. The safest approach is to get an eligibility assessment from a broker first to avoid applying with lenders whose criteria you don’t meet.

What is the minimum deposit for a bad-credit ABN car loan?

There is no universal minimum, but providing a deposit of 10–20% will significantly strengthen your application. A deposit lowers the lender’s risk by reducing the Loan-to-Value Ratio (LVR). This makes you a more attractive applicant and can unlock access to more lenders and potentially better terms, even with a poor credit history.

Can I get finance after bankruptcy or a default?

Yes, but on a case-by-case basis. Lenders want to see that the issue is resolved and in the past. Having evidence of a discharged bankruptcy or a paid default is critical. Your chances improve dramatically with a stable trading history, clean bank statements, and a lower LVR, as covered in the section above.

Your Checklist for a Bad Credit ABN Car Loan

Securing a business car loan with bad credit is achievable, but success hinges on awareness of your options and pitching your application in the right way.

You need to find the lenders that focus more on your current business stability and the deal’s structure than on past credit issues.

Follow this 4-point action plan for the strongest chance of approval:

- Know your credit file and address any adverse listings.

- Be prepared to pay a deposit to reduce the LVR.

- Apply strategically and only target lenders who are likely to approve your application.

- Use a specialist broker who understands finance for business owners.

Click below to start a conversation with our expert team, and understand your options without impacting your credit file.