Asset-based lending uses allows a business to unlock cash that is tied up in receivables, equipment, or other future cash flows to expand their working capital base.

Both liquid and illiquid assets can be used as security in various forms of commercial finance.

The result is a much more efficient use of capital and accelerated growth capacity.

However, your business model must be reliable and sufficiently profitable to absorb the costs involved.

In this article, we’ll discuss all forms of asset based lending in Australia and how you can use this to access capital quickly and supercharge your business.

Key Takeaways: Asset Based Lending

| Quick Summary | Asset-based lending allows you to use financial and physical business assets as security to access fast working capital |

| Asset Security Listings (PPSR) | Lenders rely on the Personal Property Securities Register (PPSR) to protect their interests in case of default or insolvency. |

| Borrow Against Business Receivables | Use expected future payment obligations as security to access funds now through invoice and debtor funding or purchase order finance. |

| Finance Physical Assets | Own the asset via chattel mortgages and hire purchase agreements, or lease through finance of operating lease agreements. |

What is Asset-Based Lending?

Asset-based lending (ABL) is secured commercial finance where your borrowing limit is driven by the liquidity of your assets, rather than your historical profit.

ABL providers focus on the collateral you hold right now that is unique to your business circumstances.

The approval criteria shifts from being profit driven to asset valuation.

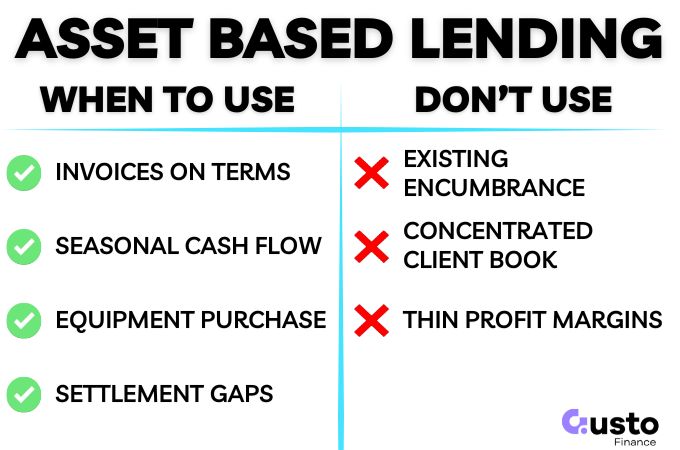

When to Use ABL

Asset based lending is a strategic cash flow solution for specific business bottlenecks, including:

- Long Payment Term Invoices: Accessing cash trapped in B2B accounts receivable.

- Seasonal Cashflow: Covering operational costs during off-peak months.

- Equipment Purchase: Funding heavy machinery without a punishing upfront cash deposit.

- Settlement Gaps: Bridging the timing difference between buying and selling property.

When to Avoid ABL

An asset based lending facility will be less suitable for the following circumstances:

- The assets used for security are already heavily encumbered.

- Your receivables book relies on a small number of major clients.

- Profit margins are thin and may not be able to absorb lending fees.

If your bottleneck is timing andy our cash is trapped in assets, ABL is often faster than re-underwriting a cashflow loan.

Understanding the PPSR

The Personal Property Securities Register (PPSR) is the national online database where security interests over personal property are recorded.

In a commercial lending context, it determines priority for payment if a business becomes insolvent.

Existing encumbrances are the most common cause of funding delays when organising an ABL facility.

If a previous supplier or an old loan still has a charge listed against your business, your new lender will block the application immediately.

Your new lender will also register their interest on this database and you need to know exactly what rights you are signing away before the funds are released.

PPSR Risk Checklist

- Confirm Clean Title if you have had previous finance. Running a search is easy and cheap and can prevent delays if a past creditor has not removed a listing.

- Check the scope of the new security registration (and seek professional advice). Security may be over a specific asset, or All Present and After-Acquired Property. The latter covers your entire business and restricts future borrowing.

- Understand PMSI: A Purchase Money Security Interest gives a lender priority over general bank debts for the specific equipment they finance.

This register is an important tool for controlling the risks for the lender and to your business.

How Asset-Based Loans are Structured

Funding is determined by the lender’s assessment of the asset value, applying an Advance Rate (LVR) they are willing to lend up to, minus any policy exceptions.

These reductions exclude ineligible assets that the lender will not lend against.

For example, invoices aged over 90 days, foreign debtors, or concentration limits where a single customer owes more than 20% of the total ledger could be excluded from the asset value.

Some useful benchmarks

- Invoice Finance: Expect an advance of 80–85% on eligible invoices, and up to 90% for the highest quality debtors.

- Asset Cash-Out: Short-term facilities against machinery usually provide ~70% of the asset’s Orderly Liquidation Value (OLV).

Cost of Finance

The headline interest rate is only one component. You also need to factor in any associated fees, which can include:

- Discount Fee: Interest rate applied to the funds you actually draw.

- Service Fee: A monthly administration fee or a percentage of total turnover.

- Setup & Legal: Valuation fees and legal documentation, which can range from $2,000 to $10,000 depending on complexity.

- Monitoring or Service Fees: Quarterly audit fees to verify the ledger quality.

Security Levers

Lenders manage downside risk through Personal Guarantees (PGs), director covenants, and strict insurance requirements.

Compare offers based on the net advance available (cash in bank) and total cost stack, not just the marketing rate.

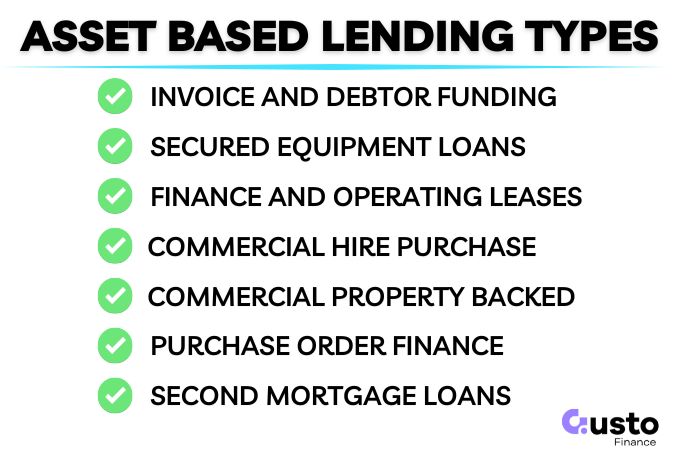

Types of Commercial Asset Based Loans

Invoice Finance and Debtor Funding

Invoice finance bridges the gap between completing work and getting paid.

It suits B2B businesses with a reliable debtor book strangled by strict 30 to 90-day payment terms.

Instead of waiting, you borrow against unpaid invoices immediately.

The flow of funds will generally follow these steps:

- Step 1 – Send the invoice to your client and sync with the lender.

- Step 2 – The lender advances up to 85% of the invoice value upfront.

- Step 3 – Once the customer pays, the lender releases the remaining balance minus fees.

Your structure also determines who controls the client relationship.

Invoice Discounting (Confidential) allows you to collect payments. Your client never knows a lender is involved.

While this is a positive to preserving your client relationships, it can be more costly for audits as your lender is removed from the process.

Or you can use Factoring (Disclosed) where the lender manages collections on your behalf and notifies your customers when there is an amount due.

This relieves admin burden but exposes your financial setup.

Standard Equipment Loans (Chattel Mortgage)

This is the most common structure for Australian businesses purchasing vehicles or heavy machinery.

Unlike a lease, a Chattel Mortgage gives you immediate ownership while the lender holds a mortgage over the goods as security.

This allows you to secure the equipment you need to grow your revenue immediately.

Because the loan is secured by the asset, interest rates are lower than unsecured options.

Lenders focus on the asset’s age, condition, and resale market value when assessing the security.

Standard vehicles and yellow goods (excavators, forklifts) are generally easier to approve.

Highly specialised or older machinery often requires a formal valuation to prove it holds sufficient security value.

The Finance Lease

Ownership isn’t always the smartest play for your balance sheet.

Under a Finance Lease, the financier purchases the asset and rents it to you for a fixed term.

This structure prioritises cash flow over equity. It preserves working capital for growth rather than locking it into a depreciating asset.

Since the financier retains ownership, rental payments are usually treated as operating expenses.

This offers tax timing benefits distinct from standard loan depreciation.

A finance lease allows your business to retain flexibility with the asset when you reach the end of the agreement period.

When the contract ends, you have three pathways:

- Return the asset to upgrade to the latest model.

- Extend the lease term.

- Offer to purchase the goods for the residual value.

You should always clarify the residual value before signing the contract. A lower monthly rental often leads to a large final payout.

Also, confirm maintenance responsibilities. While you don’t own the asset, you may still be liable for insurance and repairs.

The Operating Lease

An Operating Lease is effectively a long-term rental. You pay for usage over a set term and return the asset at the end.

Ownership never transfers to you, meaning you avoid the risk of residual value loss.

This is a suitable choice for assets with short lifespans or frequent upgrade cycles, such as IT hardware and corporate fleets.

This type of lease helps prevent your business from being stuck with obsolete technology or aging vehicles when there is a tangible benefit to staying up to date.

The total cost is often higher than owning, but you pay a premium for the flexibility to upgrade or walk away without disposal headaches.

Lenders can enforce strict return conditions for things like usage limits (like kilometer caps) and make good clauses.

Excessive wear and tear often triggers significant break costs upon return.

Commercial Hire Purchase (CHP)

A Commercial Hire Purchase puts you in the driver’s seat immediately, but the lender retains ownership until the final dollar is paid.

You hire the asset for a fixed term with regular instalments.

Legal title transfers to you only after the contract ends and any residual value is paid.

This is best for businesses that require a clear path to ownership but need to spread the capital cost over several years to preserve working capital.

The timing of your tax deductions depends heavily on your accounting method.

- Accrual basis: You can typically claim the full GST input tax credit upfront.

- Cash basis: You generally claim GST progressively over the life of the loan.

You should consult your accountant before commencing a hire purchase agreement so you can forecast the cash flow impacts over time.

Unlike the lease structures, this is a hard commitment to purchase.

It lacks the flexibility of a rental where you can return the asset if workload drops.

Commercial Property-Backed Lending

Commercial real estate is one of the more powerful levers for raising significant capital at cheaper interest rates.

This form of lending secures business finance against brick-and-mortar assets rather than moving parts like machinery.

Use this for major strategic moves where longer terms are essential.

Common uses include funding business acquisitions, large-scale fit-outs, or refinancing expensive short-term debt into manageable long-term facilities.

Property lending requires a deeper assessment than equipment finance. Lenders look at:

- Valuation: A formal physical inspection and report are mandatory.

- Lease Profile: For investment properties, the financial strength of your tenants matters.

- Existing Debt: Usable equity is calculated after deducting existing mortgages.

Property-backed facilities offer the lowest interest rates and terms up to 30 years. However, the process is slower.

Settlement can take 4 to 8 weeks due to valuations and mortgage registration.

Legal fees are also higher than standard asset finance. Choose this for borrowing power and lower costs, not for speed.

Purchase Order (PO) Finance

Landing a major contract is a cause for celebration, but it often triggers a cash flow crisis.

You have the order, but lack the capital to pay suppliers to fulfill it.

PO Finance is a form trade finance that solves this by paying your supplier directly for the goods.

Lenders will scrutinise the deal itself rather than your finances.

You need a confirmed Purchase Order from a credible end-buyer (like a government body or ASX-listed retailer) and a demonstrable profit margin.

The lender will verify the legitimacy of the purchase order and your supplier’s ability to deliver.

If the transaction chain is weak, the loan is denied.

This is high-friction finance.

Documentation is heavy, fees are higher than standard working capital, and lenders usually control the final invoice settlement to ensure repayment.

It is only a realistic solution if your deal margin is healthy enough to absorb the extra cost.

If the order is varied or cancelled, the facility breaks immediately.

Second Mortgages and Caveat Loans

A second mortgage allows you to unlock property equity without disturbing your existing low-rate bank loan.

The new lender takes a secondary ranking position behind your primary bank.

This means that if you default on the mortgage and the property is sold, the primary lender is paid first and the second mortgage is paid with any funds leftover.

So it is a higher risk position from the lender’s perspective.

Business owners use these facilities when the timeline is short.

Banks can take weeks, and sometimes months to approve a top-up loan, and many will not allow borrowing for business purposes at all.

However, private lenders can fund a caveat loan in days.

Common uses of a second mortgage includes:

- Injecting urgent working capital

- Seizing immediate expansion opportunities

- Bridging gaps while waiting for long-term facilities

The second lender is subordinate, meaning they are last in line to be paid if you default.

To compensate for this risk, interest rates are significantly higher than standard mortgage rates.

Lenders will conduct strict diligence to confirm you have enough usable equity and may require a deed of priority from your first bank to proceed.

These loans are strategic bridges, not long-term solutions.

Never sign without a concrete exit plan, such as selling the asset or refinancing once financials improve.

Without a viable exit, high interest costs will rapidly destroy your equity.

Frequently Asked Questions

Do I need to worry about the PPSR if I’m the asset-based borrower?

Yes, absolutely. Lenders use the Personal Property Securities Register (PPSR) to legally claim priority over your assets. Before applying, you should check for old registrations that could block funding. Crucially, ensure your new lender registers a security interest only over the specific equipment being financed, rather than an All Assets charge over your entire business which restricts future borrowing.

What happens if I default on an asset-based facility?

The lender will issue a formal default notice and can enforce their security interest to recover the debt. This usually involves repossessing and selling the asset to pay out the loan balance. Because the lender holds a mortgage or charge over the specific goods, they can act faster than with unsecured debts.

Summary

Asset-based lending turns your balance sheet items like invoices, equipment, or property into immediate borrowing capacity.

It converts idle value into the working capital you need to grow.

Success requires strict attention to the non-negotiables.

Always verify a clean PPSR title, calculate the true total cost including reporting fees, and define your exit strategy before you sign.

If speed is critical or the deal has moving parts, speak to a specialist broker first.

We can sanity-check your structure and compare lender options to help you secure the right funding without hidden risks.